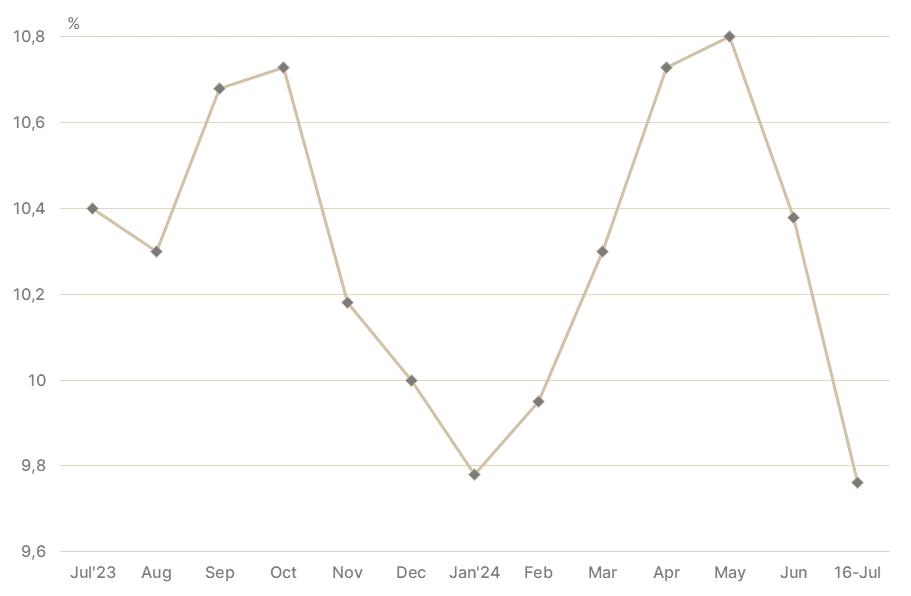

The decline of more than 140 basis points in South Africa’s ten-year bond yield in the aftermath of the recent elections holds the promise of hastening the imminent lowering of the Reserve Bank’s repo rate.

A positive medium to long-term relationship exists between money market rates and long-term interest rates. Should the declining trend in the long-term bond yield continue, it would serve as a clear signal that the repo rate and commercial lending rates are falling significantly behind the curve.

The chances for an easing of lending rates happening sooner rather than later have also improved for other reasons, mainly because of further declines in the producer price index (PPI) and the food price index, both of which act as leading indicators of the consumer price index (CPI).

Exhibit 1 | South Africa’s 10-year bond yield

Note: Monthly Average. Source: Trading Economics. Data as at 16 July 2024. Past per Past performance is not a reliable guide to future performance. For illustrative purposes only and not indicative of any investment.

After some nervousness with an uptick in producer prices in April, the PPI declined again in May, with the latest reading of 4.6% virtually on the nose of the mid-point of the Reserve Bank’s target range for inflation. Price increases at the factory gate are also lower than the consumer price index, which remains marginally above 5%, but also comfortably within the Reserve Bank’s target range for inflation (3% to 6%).

Both the PPI and the CPI have been within the inflation target range for a year and millions of indebted South Africans are eagerly awaiting a departure from a restrictive monetary policy approach, which started at the end of 2021.

Global capital market approval of GNU

Apart from the larger appetite amongst global fund managers for South Africa’s government bonds, the domestic equity market and the rand have also benefited from the historic transition to a government of national unity (GNU) that is committed to preserving South Africa’s democratic constitution and the principle of private property rights. Between mid-April and 16 July, the JSE All Share Index (ALSI) rose by more than 11%.

The recent performance of the rand has also been impressive. Between the 1st of March and the end of June, none of the 16 key currencies monitored by Currencies Direct outperformed the rand against the US dollar, with even the Euro, the Chinese yuan and the Japanese yen taking a hit against the world’s dominant currency.

This time around, rand strength was not based on any relative weakness in the US dollar’s value, as the dollar index (DXY) strengthened by almost 2% to 105.9 over the past four months, leaving most of the world’s key currencies floundering.

Although the rand is likely to remain volatile against the dollar, several leading financial institutions are predicting a value of below R18 by the end of the year. A stronger and less volatile rand exchange rate will place further downward pressure on inflation, which could eventually lead to a series of interest rate declines in 2024.