Monthly macro and economic insights report

Our monthly To the Point column by economist Dr Roelof Botha offers in-depth analysis and commentary on the latest economic trends, market developments, and financial news. Designed to keep you informed and ahead of the curve, each edition delves into key economic indicators, explores their impact on global and local markets, and provides insights to help you navigate the ever-changing economic landscape

October 2025

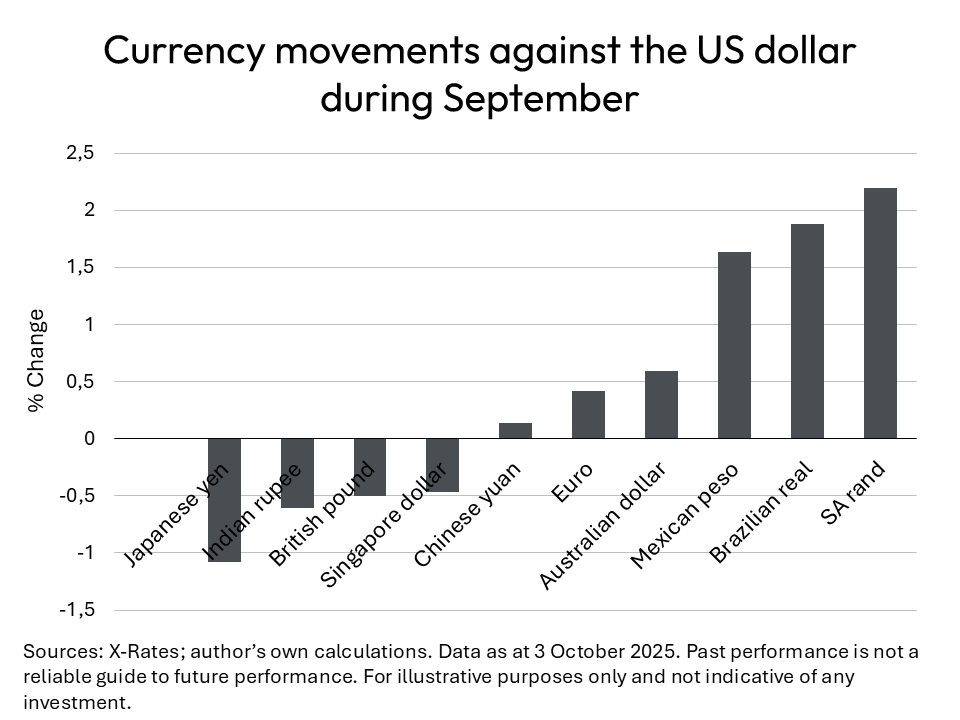

Rand strength continues in September

South Africa’s currency enjoyed a splendid run during the first month of spring, outperforming every currency of note against the US dollar (including the Euro, the Chinese yuan, and the British pound). The rand has strengthened by more than 9% against the greenback since the beginning of the year, and only four other currencies[1] have a better record during 2025 (namely the Brazilian real, the Euro, the Mexican peso, and the Polish zloty).

During September, the average appreciation of the 16 key currencies covering the advanced economies and emerging markets was marginally positive (at 0.1%)[2], but the rand flexed its muscles with a strengthening of 2.2%, followed by the Brazilian real in second place and the Mexican peso in third place. A solid performance of South Africa’s balance of payments during the first half of 2025 assisted the strength of the rand, whilst the country’s gold and foreign exchange reserves remained close to the new record high of R1.25 trillion reported in April.

The rand’s performance was especially impressive against the background of a stable US dollar index, which ended September on 97.8 – unchanged from a month earlier. The dollar remains under pressure as a result of lower bond yields and weakness in several key economic indicators, including the services sector purchasing managers’ index (PMI). Furthermore, data from the International Monetary Fund (IMF) shows a retreat in the share of US dollar-denominated assets held by other central banks, namely from 57.8% of global foreign exchange reserves in the first quarter of 2025 to 56.3% in the second quarter – the lowest since 1994.

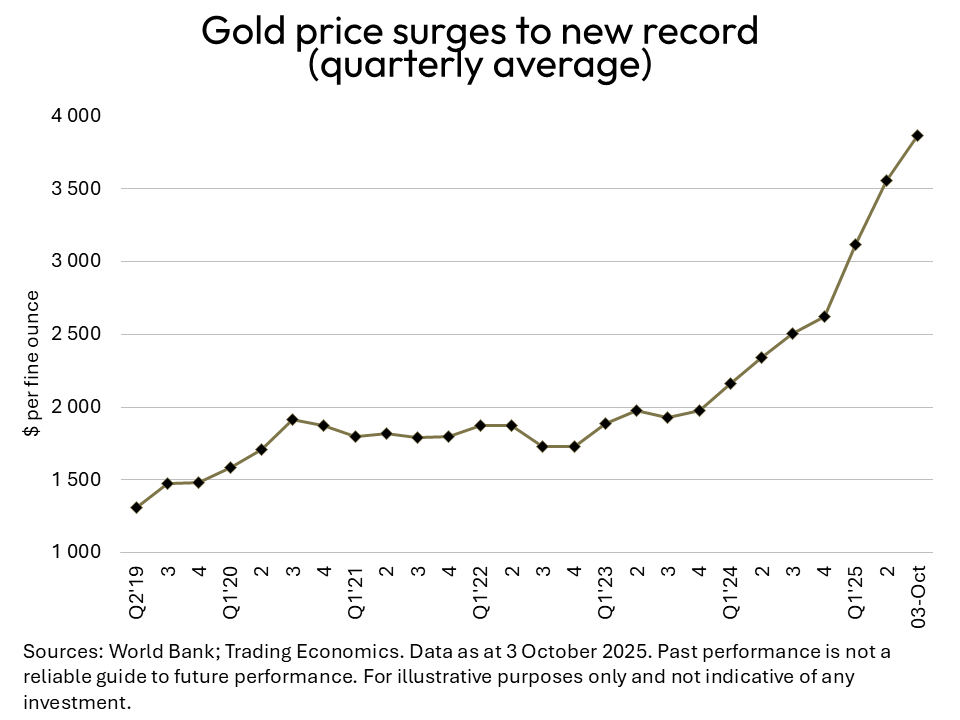

Gold price aiming at $4,000

The gold price continues to soar to new all-time highs, setting its sights on the $4,000 mark. The rise in the gold price has been nothing short of spectacular, with an increase of 133% from its level three years ago. The latest surge occurred in the wake of an interest rate cut in the US, which had been anticipated for several months.

New employment openings in the US, as measured by the Labour Department’s Bureau of Labour Statistics, only increased marginally in August while hiring declined. Households in the US are also becoming more pessimistic about the labour market. A survey from the Conference Board published at the end of September showed the share of consumers viewing jobs as “plentiful” fell to the lowest level since early 2021. These data sets point to rising unemployment, which has reinforced expectations of two more Federal Reserve rate cuts before the end of the year (despite inflation remaining marginally above the Federal Reserve’s target rate of 2%).

Gold’s record-high has resulted in a positive spin-off for platinum, with the jewellery demand for this precious metal having been boosted in recent months. The resources sector on the JSE has also reaped the rewards, with the Resource-10 index more than doubling since the beginning of the year. With the yield on 10-year US Treasury bonds having declined by 70 basis points since mid-January and dovish expectations from the Federal Reserve, investor appetite has turned to safe havens, which could boost gold and platinum even further.

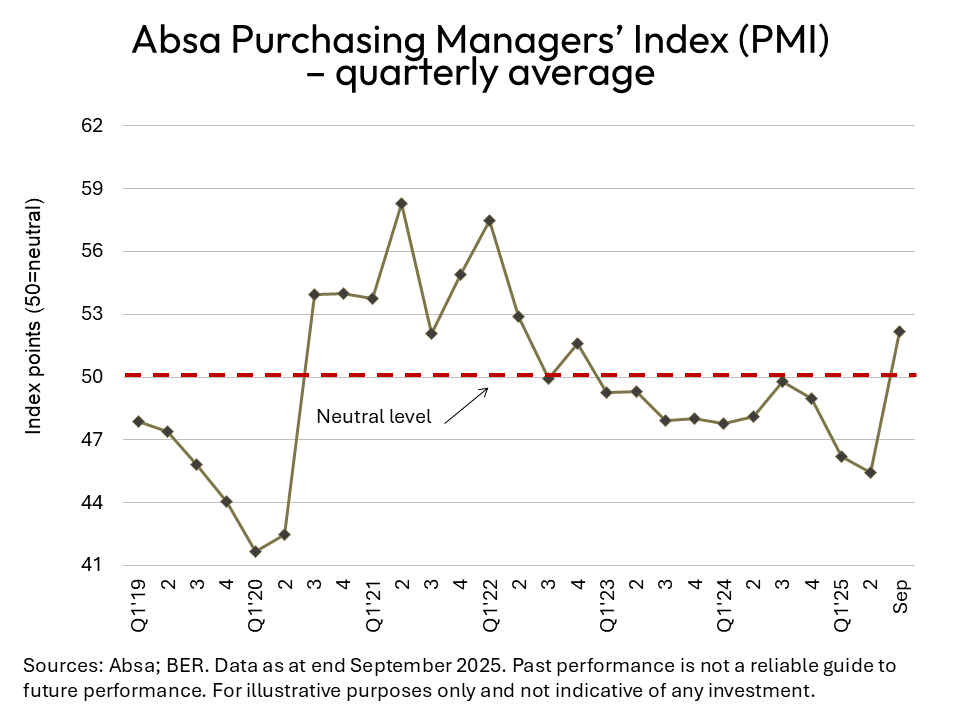

Absa PMI hits three-year high

The strong performance of retail trade sales during the first three quarters of 2025 seems to have filtered down to the manufacturing sector, with the Absa Purchasing Managers’ Index (PMI) rising to a level of 52.2 in September 2025. This is its highest end-of-quarter reading in more than three years. The Absa PMI is surveyed monthly by the Bureau for Economic Research (BER).

No doubt the lowering of the prime overdraft rate from 11.75% a year ago to 10.5% currently, also contributed to a sufficient expansion of consumer demand to warrant a more positive mood amongst factory owners. According to Absa, the domestic market drove the recovery as global demand has remained under pressure as a result of steep US tariffs, a challenging trading environment, and lingering S.A. port issues. The rebound in local demand was made possible by strong growth in business activity and new sales orders

Despite the welcome improvement in the rate at which containers are being handled at South Africa’s ports, other logistical obstacles related to export paperwork delays have come to the fore. The outlook for expected business conditions six months ahead is also under pressure, mainly due to growing uncertainty about global headwinds caused by the so-called tariff wars, combined with relatively weak global growth, especially in China.

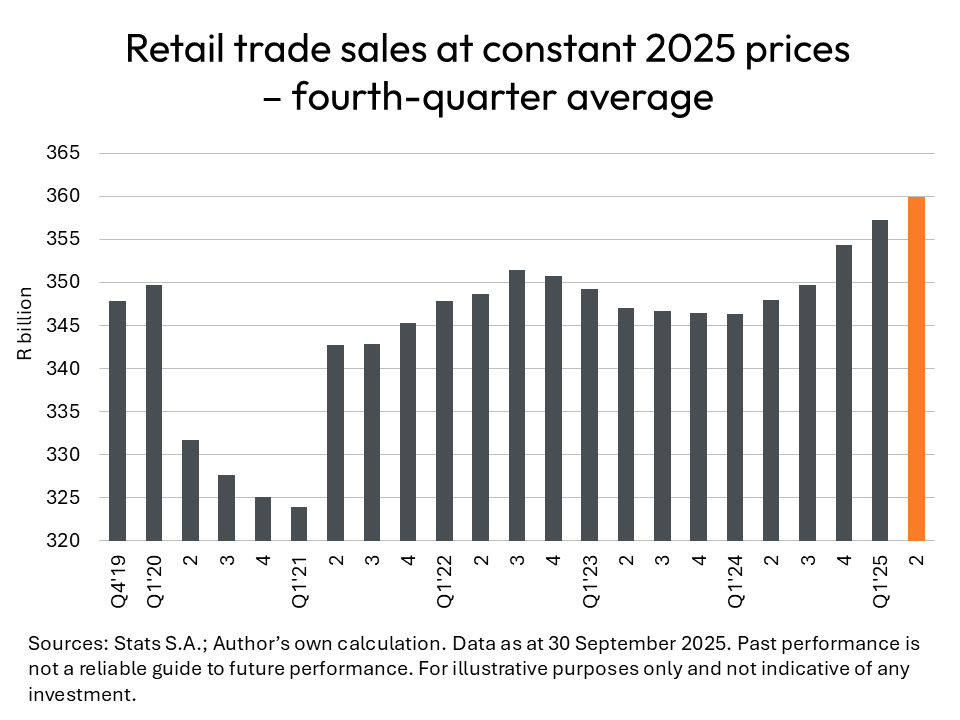

Retail trade boosted by lower prime rate

One key economic sector that has prevented the economy from slipping into recession is retail trade, which also dovetails into the hospitality industry. The latter has experienced a strong recovery from the lockdowns imposed during the worst of the Covid-19 pandemic, as reflected in a virtual full recovery of tourist arrivals.

The average annualised growth in total retail sales during the first half of 2025 stands at 5.7% (in nominal terms). This is 90% higher than the current consumer inflation rate of 3% and, if sustained, will lead to a total sales value of close to R1.6 trillion for the full year. The best performing types of retailers during the second quarter of 2025 were textiles & clothing, pharmaceuticals & toiletries, general dealers, specialised food & beverages, and household furniture & appliances.

Over the past six months, a fortuitous combination of marginally lower interest rates, a welcome increase in average remuneration levels, and lower inflation has managed to lift household consumption expenditure by a healthy margin.

The combined national accounts sector for retail trade, wholesale trade, hospitality and catering contributes close to 14% of the country’s total output (before government taxes and subsidies) and may become only the third sector to break through the R1 trillion mark for value added in 2025. The other two are personal services and financial intermediation, real estate & business services.