Monthly macro and economic insights report

Our monthly To the Point column by economist Dr Roelof Botha offers in-depth analysis and commentary on the latest economic trends, market developments, and financial news. Designed to keep you informed and ahead of the curve, each edition delves into key economic indicators, explores their impact on global and local markets, and provides insights to help you navigate the ever-changing economic landscape.

Gold remains in demand

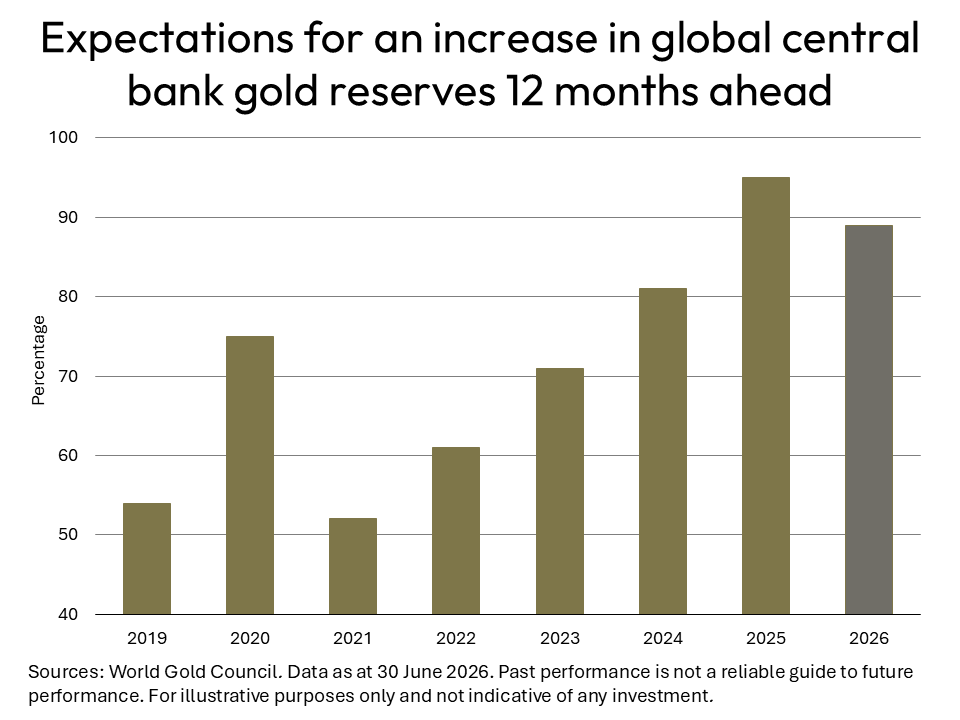

Gold-producing countries will take heart from the 2026 survey of gold reserves amongst central banks (conducted by the World Gold Council), which confirms a strong intention to continue lifting their gold reserves.

Participation in the survey was robust and representative of the overall central bank community, both geographically and in terms of gold owned. The latest survey drew in a record 76 responses, with 18 from advanced economies and 58 from emerging markets and developing economies (EMDEs), with no significant deviation having been observed between these two groups.

According to the survey, central banks continue to hold favourable expectations on gold, with 89% of respondents indicating that global central bank gold reserves will increase over the next 12 months. Although this figure is marginally lower than in 2025, this bullish gold sentiment is 71% higher than in 2021 and 21% higher than the average expectation of an increase over the past eight years.

Conversely, the majority of respondents (74%) expect lower US dollar holdings within global reserves over the next five years. This view may, however, be tempered during the second half of the year, due to higher inflation in the US and a stronger US dollar. Respondents also believe that the share of other currencies, such as the euro and renminbi, will remain unchanged over the next 12 months.

The key considerations for central bank gold holdings are portfolio diversification and hedging against inflation and geopolitical risk, with the latter having been quite prominent since the Russian invasion of Ukraine and the recurring hostilities in the Middle East.

Construction edging forward

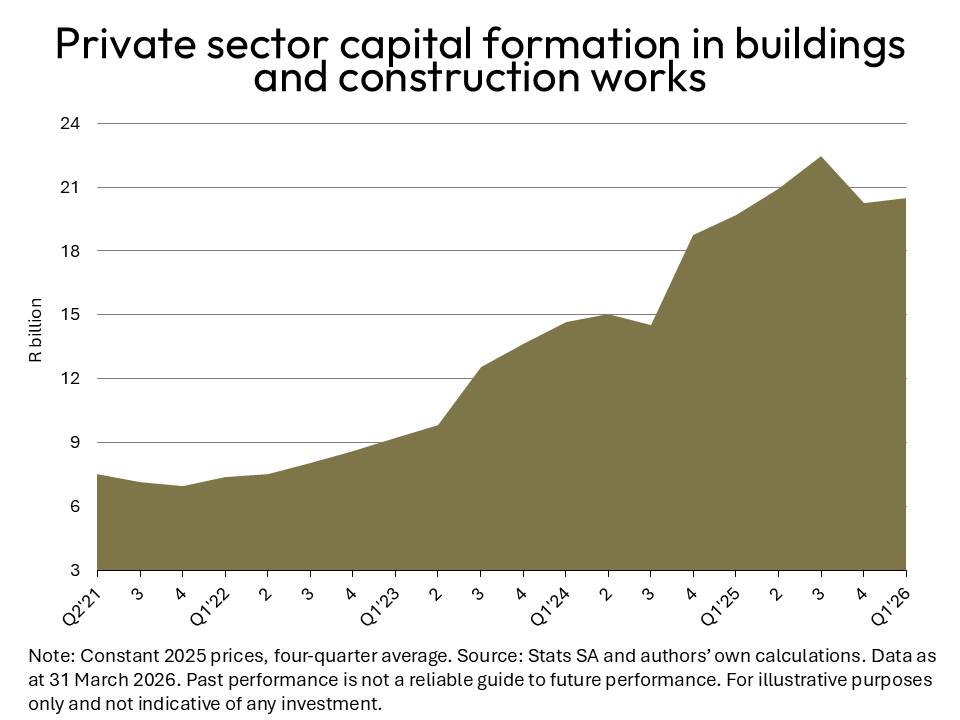

According to the latest private sector capital expenditure survey conducted by Statistics S.A., the construction sector remains on a modest growth path.

Although the seasonally-adjusted value of capital formation in new buildings and construction works during the first quarter of 2026 only increased by 1.3% (in real terms from its level a month earlier), it has risen by more than 9% (in real terms) since interest rates started to decline at the end of 2024.

Renewed activity in the construction sector (which is labour-intensive) is most welcome, especially due to its high employment multiplier effect and the dire need for repairing and expanding the country’s infrastructure. The positive capital expenditure trend emanating from the Statistics S.A. survey is in line with a modest improvement in the Afrimat Construction Index (ACI) for the first quarter of 2026, which consists of 10 different indicators relevant to construction activity.

The ACI was boosted by increases in the values of construction works and buildings completed, whilst employment and sales of building materials also improved. It is also encouraging that employment levels in the construction sector have managed to outperform job creation in most other sectors, with 74,000 more jobs in the first quarter of 2026 than a year ago.

According to a report published by Industry Insights, overall construction tender activity in South Africa increased by 11.4% year-on-year in the first four months of 2026. KwaZulu/Natal, the Eastern Cape and North-West showed notable increases thus far in 2026. Although smaller projects remain hamstrung by governance constraints at municipal level, progress has been achieved with relatively large projects, especially in energy.

Salary increases outstrip inflation

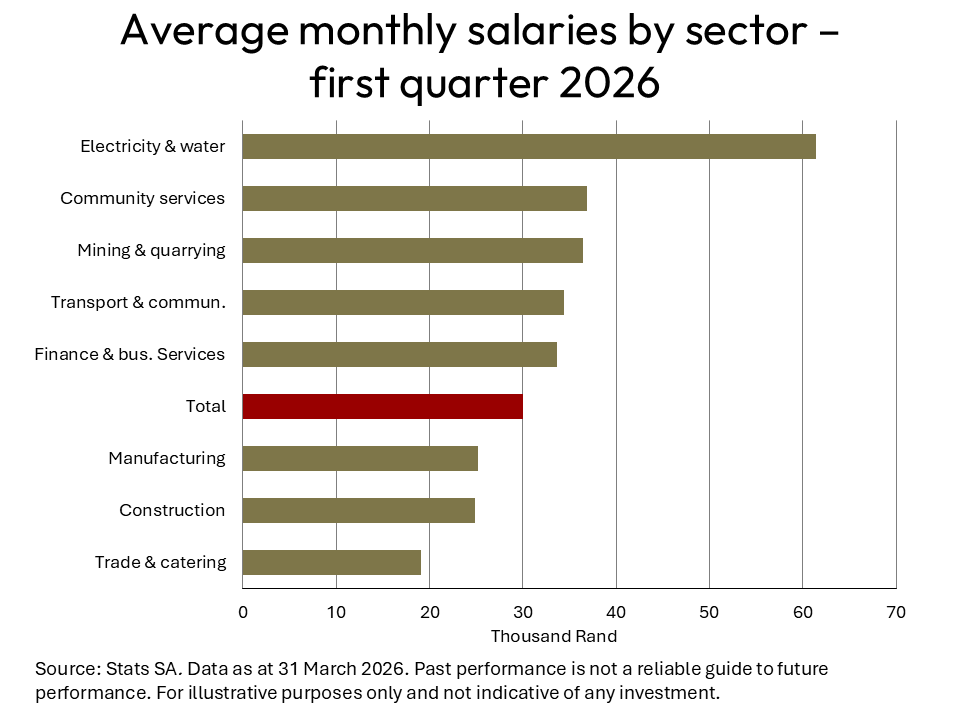

During the first quarter of 2026, the nominal year-on-year growth in average monthly salaries outpaced the current annualised change in the consumer price index (CPI) by a considerable margin. Between January and March, the average rate of consumer inflation was 3.2%, compared to an annualised increase of 5.9% in the average salary in South Africa’s formal sectors.

Workers in the construction sector were the only ones that did not record salary increases well above the CPI, namely 3.4%. In sharp contrast, workers in the sector for electricity, water and gas recorded an average salary increase that was more than three times higher than the rate of inflation, namely 10.3%. This sector remains the one with the highest level of labour remuneration, namely an average monthly salary of R61,400.

The fact that workers in the mining and quarrying sector received the second highest annualised salary increase (7.7%) can, to a large extent, be attributed to the record high prices for precious metals that existed during the first quarter of 2026.

When compared to other indicators of income levels in South Africa, the national average monthly salary of R30,000 is significantly lower than that of first-time home buyers (FTBs). According to data from BetterBond, which is one of the country’s largest bond originators, the average income of FTBs was R49,200 during the three months ended March 2026 – 5% higher than in the first quarter of 2025.

Tourism recovery complete

South Africa’s tourism industry has shown scant regard for the global tourism hiccup caused by a combination of hostilities in the Middle East and soaring fuel prices.

According to the latest data from UN Tourism, the conflict in the Middle East is likely to reduce international tourist arrivals in 2026 to below 3%, with almost zero growth having been recorded in March. The global travel and tourism industry has been hit hard by the spike in aviation fuel and air fares. On top of more expensive travel, the aviation industry has also been hurt by uncertainty about air connectivity and reduced flight capacity.

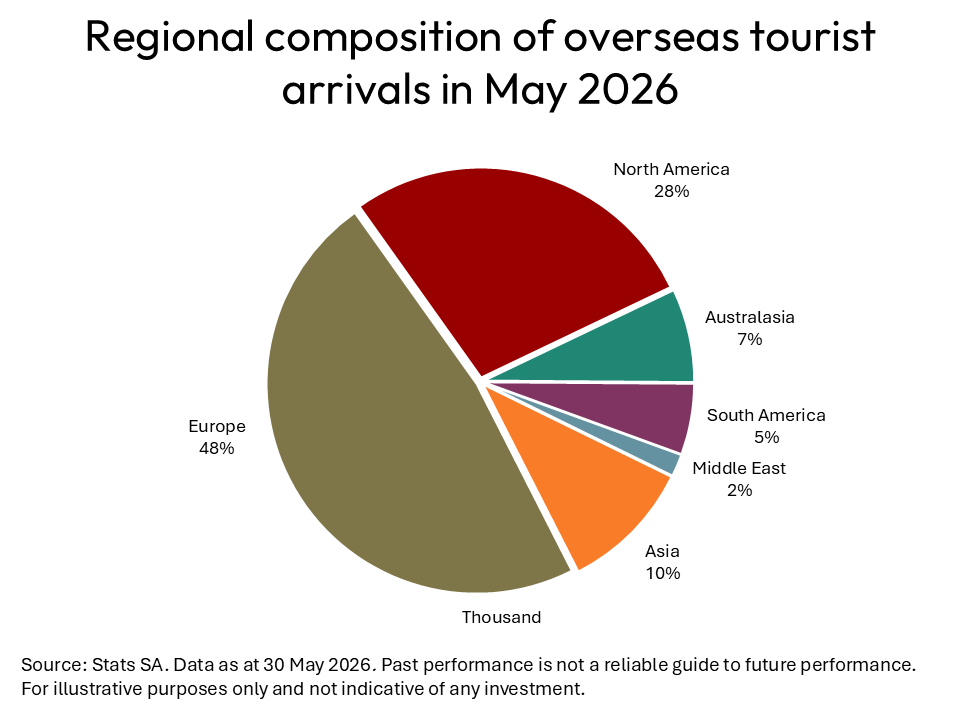

In South Africa, however, the arrivals of overseas visitors during the first five months of 2026 increased by 6.5% (year-on-year), a marked improvement on the 4.8% year-on-year growth recorded between 2024 and 2025. During May 2025, the number of overseas visitors to South Africa finally managed to surpass the level achieved in the same month before the lockdown imposed by the Covid-19 pandemic.

The UK continues to occupy the top spot in terms of overseas arrivals, with the US hot on its heels, followed by Germany, the Netherlands, France and Australia. From a regional perspective, Europe continues to dominate, with North America in second position. An interesting observation from the May data on international tourism compiled by Statistics SA is the dominance of arrivals from countries classified as free enterprise democracies. This group of countries accounted for 96% of overseas arrivals to South Africa.