For decades, portfolio construction has followed a familiar blueprint by splitting investments into clearly defined asset buckets, namely, equities for growth, bonds for income and stability, and cash for liquidity. Then allocate capital across these, typically within a 60/40 framework. Hedge funds, when included, were generally treated as small satellite allocations, often viewed with caution due to perceived complexity or risk. This is also highlighted in Regulation 28, which allows a maximum allocation of 10% to hedge funds.

The limitation of the traditional approach

This traditional framework, while simple, is increasingly misaligned with how portfolios behave in modern markets. As hedge funds have become more accessible and 100% regulated, particularly in South Africa, they are steadily moving from the periphery into the core of portfolio construction. This shift calls for a more fundamental rethink: away from asset labels and toward understanding the economic role each investment plays in delivering client outcomes.

The limitation of the traditional approach lies in its focus on what an asset is, rather than what it does. More importantly, this approach does not adequately address clients’ real needs. Investors are not ultimately concerned with whether their portfolio outperforms a benchmark each year; they are concerned with whether it can deliver consistent income, preserve capital, and sustain them over time. This is where a shift to economic roles becomes critical.

A role-based framework

This approach reframes portfolio construction around the function each investment serves, and instead of allocating capital to asset classes, allocations are made based on outcomes. In the latter, investments are grouped into broad roles, namely income, inflation protection, liquidity, capital preservation, and growth. Each role contributes to the overall behaviour of the portfolio, and importantly, multiple asset types (including hedge funds) can fulfil more than one role depending on their style/strategy.

Hedge funds play a particularly important role in delivering income stability.

Unlike traditional equities, which can experience large price swings and unpredictable dividend streams, many hedge fund strategies are designed to produce absolute returns with controlled volatility. Through differentiated strategies such as long/short, market-neutral and fixed income, they aim to generate consistent returns regardless of broader market movements. This makes them well-suited to forming a central component of a portfolio’s return engine, especially for clients with an income need.

Hedge funds significantly improve the risk profile of a portfolio. One of their key benefits is the ability to reduce overall volatility and limit drawdowns. Because many strategies have low correlation to traditional asset classes, they introduce a different source of return, one that is less dependent on market direction and more reliant on manager skill and strategy execution. This diversification effect becomes especially valuable during periods of market stress, when equities decline, and traditional defensive assets may not provide the expected protection. By smoothing the return profile and reducing the severity of losses, hedge funds help create a more stable investment experience for clients.

This stability is particularly relevant when considering longevity risks, in other words, the risk that a client outlives their capital. For clients drawing an income (retirees), the sequence of returns matters greatly. Large losses early in retirement, combined with ongoing withdrawals, can permanently impair a portfolio’s ability to recover. Traditional portfolios that rely heavily on equities for growth expose clients to this risk, as market downturns can coincide with periods when capital is being actively drawn down.

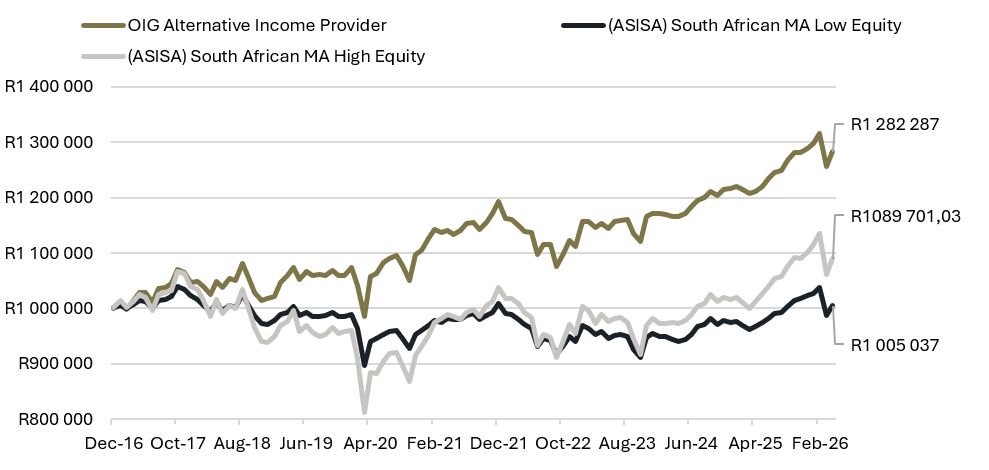

The above is illustrated in the graph below. The graph compares the return profile of the OIG Alternative Income Provider portfolio with a traditional multi-asset low equity fund and a multi-asset high equity fund.

- The OIG Alternative Income Provider portfolio is built for clients with an income need, and it has a core allocation to hedge funds.

- The ASISA Low Equity has an average equity exposure of 30% and no allocation to hedge funds.

- The Multi-Asset High Equity has an average equity exposure of 70% and no allocation to hedge funds.

For this example, all portfolios have a starting capital amount of R1,000,000 invested in April 2016 and have an annual portfolio drawdown of 6% (R5000 per month) with an escalation of 6% each year.

Exhibit 1 | Hedge Fund allocation versus traditional portfolio

Source: Morningstar. Data as at 30 April 2026. Past performance is not a reliable guide to future performance. For illustrative purposes only and not indicative of any investment

As can be seen in the graph,

- There is capital growth despite monthly income.

- The OIG solution comfortably delivers growth in assets despite the monthly drawdowns.

- The OIG portfolio that has an allocation to hedge funds comfortably outperforms the other two portfolios, neither of which has an allocation to hedge funds.

Incorporating hedge funds into the core allocation helps mitigate not only sequencing risk but also longevity risk due to a more consistent return profile. It reduces the likelihood of significant early drawdowns, and its emphasis on capital preservation helps maintain the asset base from which income is generated. This creates a more sustainable withdrawal framework, improving the probability that the portfolio can support the client throughout their lifetime.

In closing

When portfolios are restructured around economic roles rather than asset buckets, the overall design naturally evolves. Instead of a rigid 60/40 split between equities and bonds, a more balanced and functional allocation exists in which hedge funds form a core stabilising component alongside traditional assets. Equities still play an important role as drivers of long-term growth, but they are no longer the dominant foundation. Instead, they are complemented by strategies that deliver smoother, more predictable outcomes.

Ultimately, the shift from asset buckets to economic roles represents a more sophisticated and client-centric approach to portfolio construction. It recognises that the true objective of investing is not simply to maximise returns, but to deliver a reliable combination of income, growth, and capital preservation over time. By placing hedge funds at the centre of this framework, portfolios are more resilient, less volatile, and better aligned with the real-world needs of their clients.