The positive impact of lower interest rates on consumption expenditure by households, combined with the price increases of precious metals, has provided some cheer for the National Treasury.

One of the highlights of the 2025 Medium-Term Budget Statement (MTBS) presented to Parliament on 12 November was an increase of more than 9% in revenue collection for the first six months of the 2025/26 fiscal year. Revenue collection reached R925 billion, compared to the same period last year and exceeding earlier budget estimates.

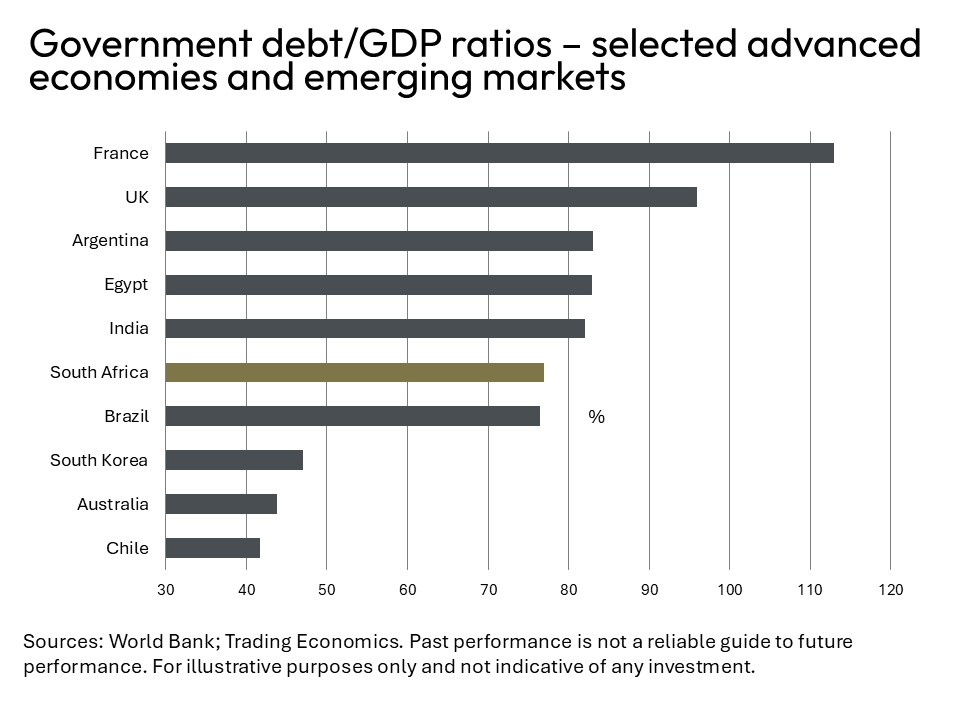

The government’s debt-to-GDP ratio is expected to stabilise at below 78% during the current fiscal year and then start declining.

After months of speculation, Finance Minister Enoch Godongwana also announced an amendment to the Reserve Bank’s inflation target, which was met with mixed reaction. According to the Budget Statement, the purpose of the lower target of 3%, with a tolerance of 100 basis points, will assist in securing lower inflation and supporting higher long-term economic growth.

Unfortunately, this optimistic scenario will not materialise soon, as acknowledged by Finance Minister Godongwana. He warned that the reduction in the inflation target to 3% would (over the short- to medium term) lead to lower nominal GDP, in turn resulting in lower revenue projections and a less favourable debt-to-GDP ratio.

The MTBS also acknowledge the presence of risks that could push local inflation higher, especially geopolitical tensions, exchange-rate depreciation and lingering risks from elevated administered prices and animal disease outbreaks. The inflationary impact of elevated wage settlements should be added to this list, although it was not addressed in the MTBS. If any of these risks materialise, the lower GDP scenario could persist for an extended period.

Another point of concern is the lowering of the National Treasury’s GDP growth forecast for 2025 to 1.2%, compared to 1.4% in the May main budget (which was delayed twice, due to disagreement in the GNU over a proposed VAT increase). The lack of measures aimed at lifting the country’s economic growth rate to a level that is commensurate with increased per capita disposable incomes is also worrying, as the National Treasury does not expect GDP growth to rise above 2% per annum over the medium term.

Other key aspects of the MTBS include:

- Progress with the government’s Targeted and Responsible Savings (TARS) programme aimed at eliminating waste and inefficiency in government spending and eliminating the phenomenon of so-called ‘ghost workers’

- Rising primary budget surpluses are expected to gradually reduce debt and debt-service costs.

The positive impact on South Africa’s sovereign risk premium following the country’s removal from the grey list of the Financial Action Task Force (FATF) was also pointed out. This is expected to lead to further declines in South Africa’s long-term bond yields, which will lower the government’s borrowing costs. The possibility of a sovereign ratings upgrade by either S&P Global or Moody’s was also mooted. Both of these ratings agencies will assess the quality of South Africa’s long-term government bonds before the end of the year.