Monthly macro and economic insights report

Our monthly To the Point column by economist Dr Roelof Botha offers in-depth analysis and commentary on the latest economic trends, market developments, and financial news. Designed to keep you informed and ahead of the curve, each edition delves into key economic indicators, explores their impact on global and local markets, and provides insights to help you navigate the ever-changing economic landscape

Progress with development indicators

South Africa’s General Household Survey (GHS) for 2025 was published by Statistics SA during May, confirming progress with several development indicators and providing useful information on regional socio-economic trends.

An outstanding feature of the latest GHS is the steady improvement in educational attainment. The proportion of people aged 20 and older with at least a National Senior Certificate (grade 12) has increased from 30.7% in 2002 to 53.5% last year. Following the introduction of a Social Relief of Distress (SRD) grant in 2020, more than 50% of households are now benefiting from the country’s comprehensive social welfare system, although salaries and wages remain the main source of income for 54.3% of households.

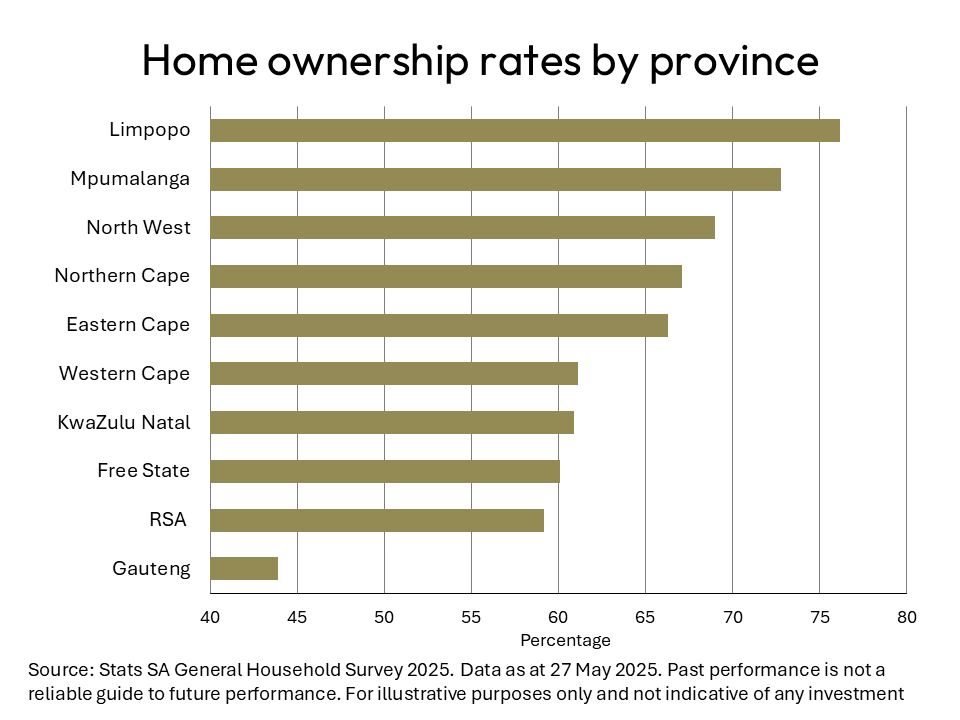

Data relating to the regional distribution of dwelling units by tenure status reveal a predictable inverse relationship between ownership levels and average house prices. The province with the largest weighting in the Residential Property Price Index (RPPI – published by Stats SA), namely Gauteng (39.1%), had the lowest provincial level of home ownership at 43.9%. The Western Cape and KwaZulu-Natal, which have the second and third largest weighting in the RPPI, also had lower home ownership levels than five of the other six provinces.

For the whole of South Africa, the home ownership rate stands at 59.2%, which compares reasonably well with many key trading partners. According to the World Population Review, South Africa’s home ownership rate is marginally lower than that of the Netherlands, Brazil and Kenya, but higher than the rates in Germany, Argentina and Nigeria.

Good news from Moody’s ratings

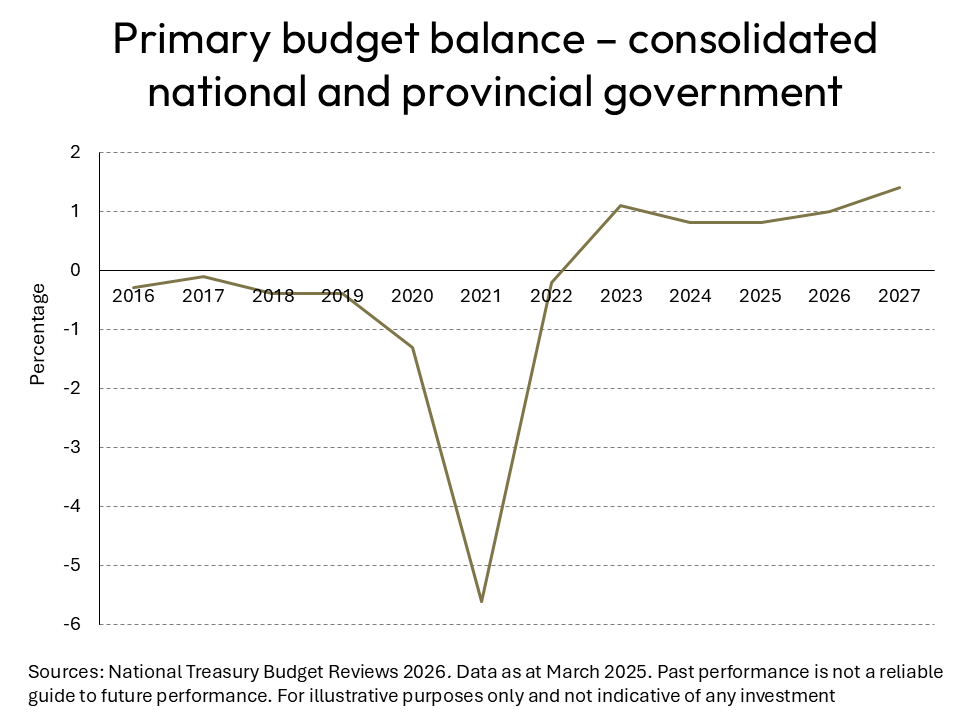

Progress with the National Treasury’s long and arduous path to fiscal stability has paid a welcome dividend in the form of a revision by Moody’s Ratings of the country’s sovereign credit rating outlook from stable to positive, while affirming the rating itself at Ba2.

Although South Africa’s rating remains in sub-investment grade territory, Moody’s Ratings has now signalled that an upgrade is possible if the recent improvement in the public finances and economic reforms persists. In its reaction to the good credit rating news, the National Treasury pointed out that the decision came during a period of negative ratings pressure, with the outlook for several sovereign ratings having been downgraded since the start of the Middle East conflict.

Viewed from the perspective of the latest national budget, the positive move in the creditworthiness of South Africa’s government bonds is no surprise. According to the latest statistical tables accompanying the annual budget, the return to a primary budget surplus (revenue minus non-interest expenditure) is picking up steam.

In a statement released by Moody’s Ratings, faith has been expressed in South Africa’s ability to keep the Government of National Unity intact and, over the longer term, to sustain progress in implementing projects aimed at infrastructure repair and expansion. Specific mention is made of the importance to crowd in substantial new private investment in the areas of energy, logistics and water.

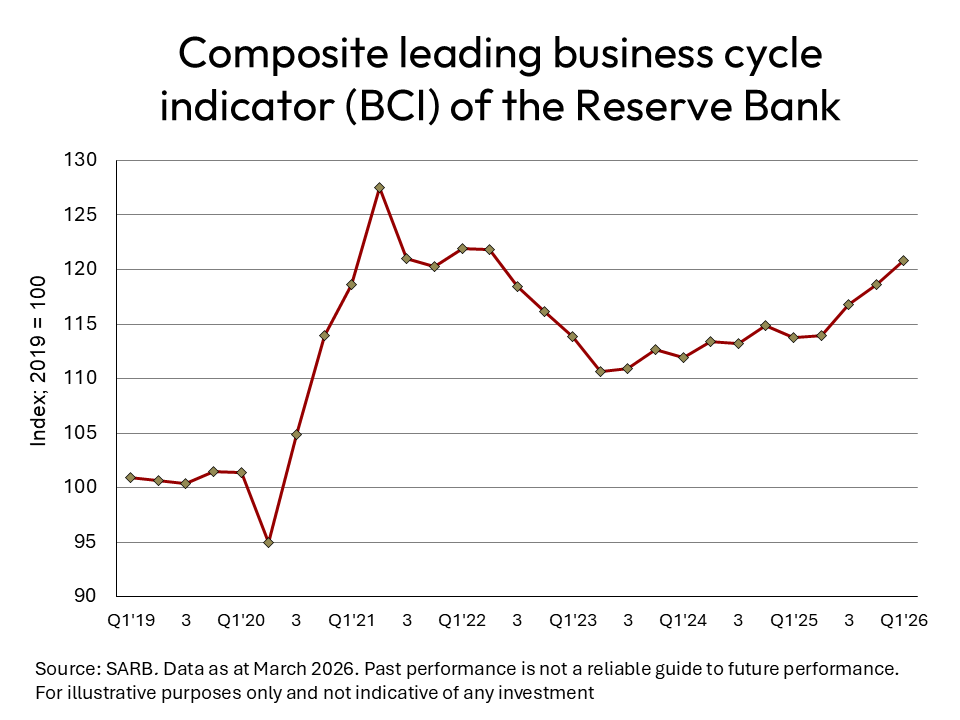

Renewed business cycle strength

The composite leading business cycle indicator (BCI) compiled by the Reserve Bank continued its upward momentum in March, increasing by 2.4% from the level in February and by an impressive 7.5% year-on-year. Six of the BCI’s seven available component time series made positive contributions during March, in contrast to a decrease in the composite leading business cycle indicator for South Africa’s major trading-partner countries.

The largest positive contributors were an acceleration of the six-month smoothed growth rate in the real M1 money supply and a widening of the interest rate spread. Other encouraging factors included increases in the number of new passenger vehicles sold (six-month smoothed growth rate) and job advertisements in the Sunday Times and Pnet, whose website attracts around 5 million visits per month.

Unfortunately, the latest reading of the coincident business cycle indicator has not been able to match the performance of the leading BCI, due to a decline in the utilisation of production capacity in the manufacturing sector. The latter has been caused mainly by insufficient demand.

The positive trend of the BCI is in sync with the latest S&P Global Purchasing Managers’ Index (PMI) for South Africa, which improved to a level of 51.6 in April – the highest reading since August 2022. A solid increase in order books and a fourth successive month of higher output volumes contributed to the positive trend in the S&P Global PMI. Staff capacity also remained on an upward trend, with employment rising for the third month running.

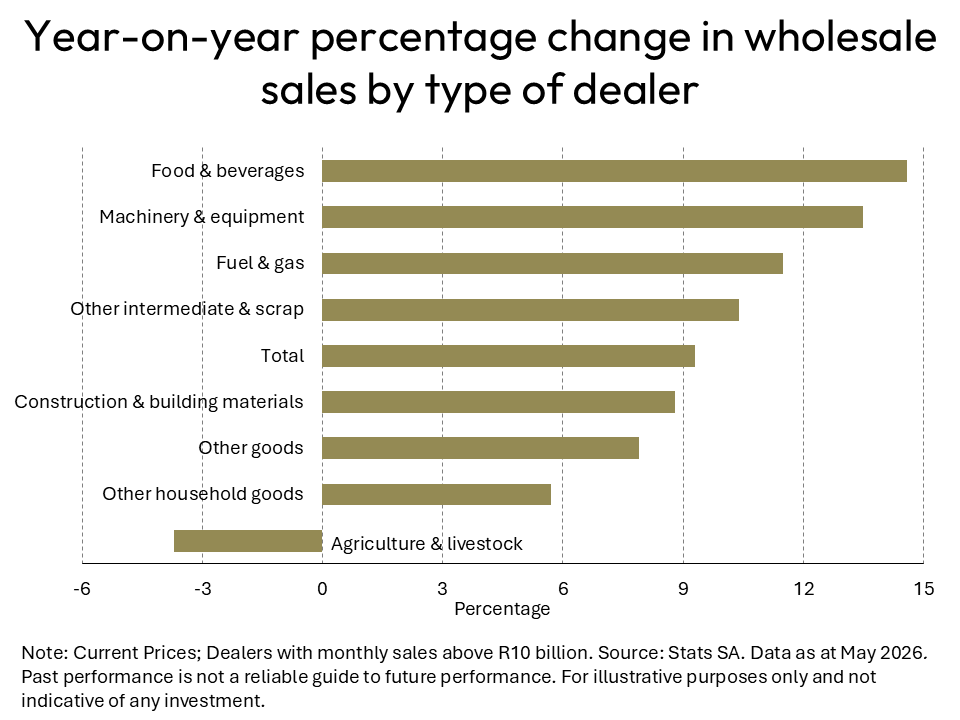

Welcome boost for wholesale trade

In March, wholesale trade sales bucked a declining trend that set in during the third quarter of 2023 to record year-on-year growth of 9.3% (at current prices). The quarter-on-quarter growth of 13.7% was even more impressive and lifted sales to above the R300 billion level for the first time since November last year (which is traditionally a bumper month, due to preparations for festive season shopping by retailers).

Between March 2025 and March 2026, nine of the twelve types of wholesale traders recorded growth, with half of them hitting double digits. These results are in line with the findings of the most recent purchasing managers’ index (PMI) for South Africa, compiled by S&P Global, which found that new orders had increased at a healthy rate. One of the reasons for the latter trend has been attributed to the closure of the Strait of Hormuz, which has led to higher maritime trade activity around the Cape of Good Hope and fears of harbour congestion.

It is especially encouraging that the wholesale trade groups for machinery & equipment and construction materials have kept pace with the overall expansion of wholesale trade during March, recording year-on-year growth rates of 13.5% and 8.8%, respectively. These two groups are inherently tied to capital formation and infrastructure development and will hopefully continue on a sustained growth path in the months ahead. In 2025, the value of total wholesale trade amounted to R3.48 trillion, and any sustained recovery of this sector is bound to filter through to other sectors, especially retail and manufacturing.