Global markets entered 2026 with increased volatility but ultimately delivered solid gains, as investors navigated a rapid succession of geopolitical shocks, shifting tariff threats, and sharp moves in commodities and interest rates. While uncertainty around US policy, central bank leadership and global trade weighed on sentiment at times, the overall backdrop remained broadly “risk‑on”, with value shares, energy and emerging markets leading performance.

Locally, South African assets extended their strong run. The FTSE/JSE All Share Index (ALSI) recorded an eleventh consecutive monthly gain, supported by surging precious metal prices and firm risk appetite toward emerging markets. The rand strengthened meaningfully, while inflation remained contained, and the South African Reserve Bank (SARB) left policy on hold as expected.

LOCAL MARKETS

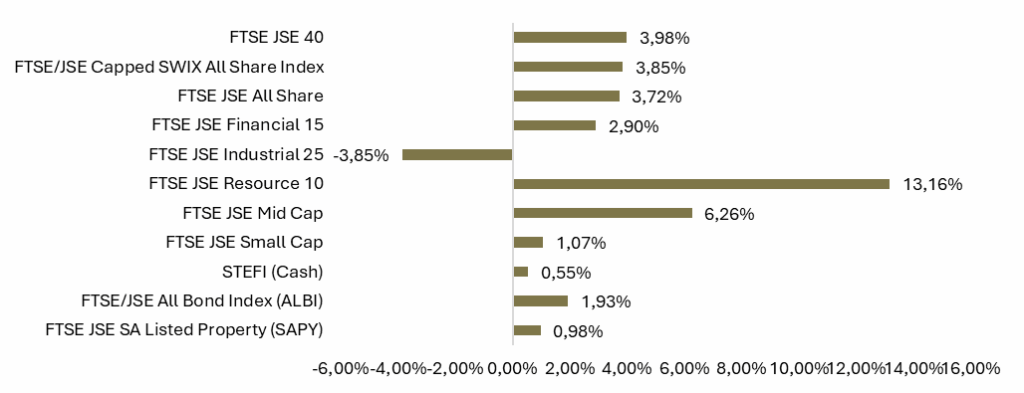

Exhibit 1 | Local Performance (ZAR) for January 2026

Source: Factset. Data as at 31 January 2026. Past performance is not indicative of future performance. For illustrative purposes only and not indicative of any investment.

South Africa

Economy

South Africa’s macroeconomic backdrop continued to improve at the start of 2026. Headline consumer inflation was up only modestly in December, printing at 3.6% (from 3.5%) in November, while core inflation rose to 3.3%. Both measures remain near the SARB’s 3% target and slightly below market expectations, reinforcing the view that inflation is broadly contained in the near term.

Improvements in global demand for commodities, alongside a more stable domestic power supply, have helped soften the drag from structural constraints, even though business conditions remain challenging.

Against this backdrop, the SARB’s Monetary Policy Committee kept the repo rate at 6.75% at its January meeting. The decision was widely anticipated and reflected a balance between a slightly improved inflation outlook and lingering uncertainty around the fiscal trajectory and global risk environment.

The rand strengthened meaningfully over the month, trading as firm as around R15.70/US$1 before ending January near R16.15/US$1. The currency was supported by broad‑based US dollar weakness, robust gains in precious metals, and growing investor recognition of South Africa’s recent progress on governance and reforms. This includes the earlier exit from the Financial Action Task Force (FATF) grey list and a sovereign rating upgrade in late 2025.

Equity Markets

South African equities started 2026 on a strong footing. The FTSE/JSE All Share Index (ALSI) rose approximately 3.7% in January, extending its impressive winning streak and again ranking among the stronger emerging market performers.

Sector performance remained highly differentiated:

- Resources surged around 13.6%, continuing to dominate the market as precious and diversified miners benefited from another powerful rally in gold, silver and platinum group metals.

- Financials gained close to 3%, supported by firmer domestic sentiment, a stronger rand and resilient bank earnings.

- Listed property (SAPY) gained almost 1%, tracking lower long‑term yields and improving perceptions of South African risk.

- In contrast, industrials had a tough month, declining by 3.85%. The sector came under pressure as rand‑hedge and consumer‑focused counters were weighed down by a stronger currency, portfolio rebalancing, and some company‑specific weaknesses.

Performance at the stock level was overwhelmingly driven by commodity‑linked counters, particularly precious metals and diversified miners. On the downside, January proved challenging for large industrial and rand‑hedge counters:

Best performers:

- Sibanye Stillwater Ltd 21.95%

- Glencore PLC 20.63%

- Implats 20.61%

- Northam Platinum Holdings 17.71%

- Goldfields Ltd 17.09%

Worst performers:

- Compagnie Financière -14.53%

- Naspers-N -10.23%

- Prosus NV -9.12%

- Mondi PLC – 8.07%

- Reinet Investments – 4.26%

Bond Market:

Domestic fixed income delivered a relatively stable performance in January. South African government bond yields were steady to modestly lower at the front end, with the 10‑year benchmark yield holding near 8% and the 20‑year yield easing to roughly 8.9%. Stronger risk appetite toward emerging markets, a softer US dollar and ongoing progress on fiscal consolidation helped anchor South African yields, even as global rates experienced bouts of volatility.

The combination of a firmer rand, improving inflation dynamics and steady policy settings provided a supportive backdrop for local bonds, which continue to offer attractive real yields versus global peers. For multi‑asset investors, South African fixed income remains a key source of income and diversification in an environment where global bond markets are still digesting the implications of higher‑for‑longer policy rates and geopolitical risk.

GLOBAL MARKETS

Global equity markets had a volatile but ultimately positive start to 2026. Policy uncertainty, around US trade and foreign relations, triggered sharp swings early in the month. Even so, economic data generally surprised to the upside, and investors shifted back toward cyclical and value‑oriented sectors, helping global markets finish January on a stronger footing.

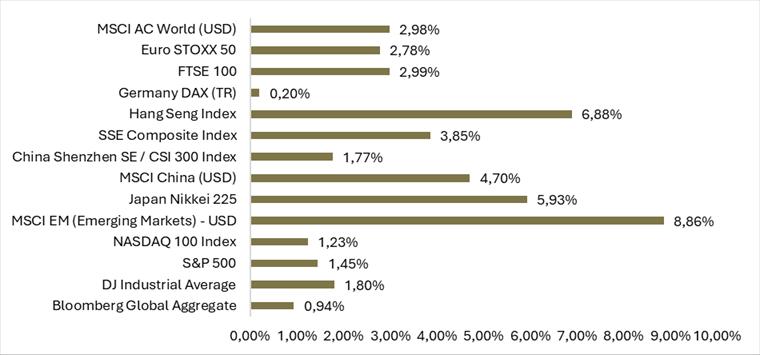

Broadly, developed market equities advanced, with the MSCI World Index rising by around 2.98% in January, while emerging markets outperformed decisively, led by strong gains in semiconductors, energy and commodity exporters. The MSCI Emerging Markets Index delivered high 8.86% gains for the month, significantly outperforming developed peers.

Exhibit 2 | Global Performance (base currency) January 2026

Source: Factset. Data as at 31 January 2026. Past performance is not indicative of future performance. For illustrative purposes only and not indicative of any investment.

United States

US financial markets were at the epicentre of January’s volatility. A combined flow of politically driven headlines periodically undermined sentiment, particularly mid‑month. Nonetheless, US equities recovered into the month‑end, and all three major indices ended higher:

- S&P 500: roughly +1.4% month‑on‑month

- Dow Jones Industrial Average: around +1.8%

- Nasdaq Composite: close to +0.9%

Several large US technology names saw share price weakness following their earnings reports; by contrast, energy shares strongly outperformed, with S&P 500 energy constituents gaining as Brent crude rallied on renewed tensions in the Middle East.

Headline CPI remained at 2.7% year‑on‑year, while core inflation printed at 2.6%, slightly below some forecasts but still above the Federal Reserve’s 2% target. The Fed’s preferred core PCE gauge also remained in the high‑2% range.

The Federal Reserve left the federal funds rate unchanged at its January meeting, emphasising a data‑dependent stance. While markets continue to anticipate some easing later in 2026, recent upgrades to US growth expectations and persistent core inflation have tempered the pace of rate‑cut pricing. The US 10‑year yield drifted higher over the month, reflecting both stronger data and an evolving fiscal and geopolitical risk premium.

Europe

European equity markets delivered another month of positive returns. The Euro Stoxx indices advanced modestly, supported by resilient corporate earnings and continued improvements in leading indicators. Germany’s DAX and broader eurozone equities benefited from stronger‑than‑expected manufacturing PMI prints and a small positive surprise in German retail sales, which rose in December rather than declining as consensus had anticipated.

United Kingdom

UK equities participated in the global rally with the FTSE 100 Index gaining close to 3% in January. Gains were broad‑based, with contributions from energy, financials and consumer names.

On the macro side, UK inflation remained elevated, with December headline CPI rising to around 3.4% year‑on‑year, while core inflation held above 3%. Nevertheless, an improvement in the manufacturing PMI, which moved further into expansion territory, and a modest recovery in house prices indicated some resilience in domestic activity. The Bank of England continues to walk a fine line between containing inflation and supporting growth, with markets still debating the timing and pace of any eventual policy easing.

Asia

Asian markets delivered strong gains in January, despite some late‑month turbulence linked to the sharp reversal in precious metal prices.

In China, equities rallied for most of the month, with the Shanghai Composite and Hang Seng indices recording solid gains before a sell‑off in the final trading session of January following a steep pullback in gold. For the month, the Shanghai benchmark still rose by 3.85%, while the Hang Seng rose around 6.9%, supported by a combination of stronger semiconductor demand, improving GDP data and renewed policy support for the property sector

In Japan, the Nikkei 225 continued its impressive run, ending January roughly 5.9% higher and setting new record highs during the month. A weaker yen, expectations of corporate governance reforms and the prospect of further fiscal stimulus underpinned investor enthusiasm, even as December inflation slowed sharply to just above 2% year‑on‑year.

Emerging Markets

Emerging market (EM) equities materially outperformed their developed peers in January. The MSCI Emerging Markets Index posted high gains, driven by:

- Semiconductor manufacturers, reflecting strong demand linked to AI and high‑performance computing.

- Miners, as precious metal and base metal prices rallied strongly.

- Broad‑based strength in commodity‑linked economies such as South Africa and Brazil.

The outperformance was reinforced by a weaker US dollar, improving growth expectations in several large EM economies, and the perception that, in many cases, the tightening cycle is already well advanced or complete.

Commodities and Currencies

Commodities delivered another volatile month, particularly in precious metals and energy. Gold extended its record‑breaking rally before retreating sharply in the final days of January. For the month, gold still delivered a decent percentage gain, supported by heightened geopolitical risk, concerns around central bank independence, expectations of further monetary easing, and robust central bank and investor demand.

Platinum group metals (PGMs) also had a strong month, with platinum and palladium rising 6.54% and 5.71%, respectively. These moves provided a powerful tailwind for South African PGM producers, which feature prominently in local equity indices.

In industrial metals, prices were mixed. Copper and aluminium weakened late in the month, reflecting some profit‑taking and lingering questions around the strength and composition of Chinese demand.

Currency markets were dominated by broad‑based US dollar weakness. The US Dollar Index fell to its lowest level in nearly four years, declining by around 1–1.5% over the month as investors reassessed relative growth and rate‑cut prospects. Emerging market currencies, including the rand, generally benefited from this backdrop, while the euro and other major currencies also gained ground against the dollar.

Outlook

January underscored how quickly market leadership and sentiment can shift when policy uncertainty collides with elevated valuations. While the month featured several episodes in which “weeks felt like decades” from a news‑flow perspective, the underlying macro environment remains more resilient than headlines alone might suggest.

For South Africa, the outlook is cautiously constructive. Reform momentum, including progress on logistics, energy and governance, as well as improved sovereign risk metrics, is gradually reinforcing the country’s medium‑term growth trajectory. Inflation is trending toward the SARB’s 3% objective, and real yields remain attractive. A supportive global backdrop for commodities, combined with a weaker US dollar and firmer EM risk appetite, continues to provide important tailwinds for local asset prices, even as domestic structural challenges persist.

Globally, growth expectations for 2026 have been revised higher across several major economies, including the US, Japan, Europe and China, reflecting a mix of fiscal support, resilient consumer demand and easing financial conditions.

In the current environment, maintaining diversification and a balanced portfolio remains essential. Equity investors should continue to hold a mix of structural growth themes alongside more cyclical, value‑oriented sectors, including financials, energy and selected commodities. On the fixed‑income side, high real yields in South Africa and other emerging markets continue to offer compelling long‑term opportunities, particularly as inflation expectations stabilise.

While short‑term market movements may remain sensitive to headlines and shifts in policy, the broader backdrop is becoming more supportive. Improving global growth prospects, accommodative financial conditions, and ongoing reform progress in South Africa provide a constructive foundation for long‑term investors. In this setting, staying well diversified, with an emphasis on quality and resilience, remains the most effective way to navigate what is likely to be another eventful year for markets.