Global markets staged a powerful rebound in April, recovering sharply from the severe sell‑off experienced in March. Improved sentiment was driven by a temporary easing in geopolitical tensions following ceasefire announcements in the Middle East, alongside a robust US corporate earnings season and renewed investor appetite for growth and technology‑linked assets. Equity markets rallied strongly across both developed and emerging markets, while the US dollar weakened and risk appetite improved more broadly.

South African assets participated in the recovery, although local equity performance lagged the sharp global rebound. While selected sectors and stocks delivered solid gains, ongoing weakness in precious‑metal prices weighed on miners and capped overall index performance.

LOCAL MARKETS

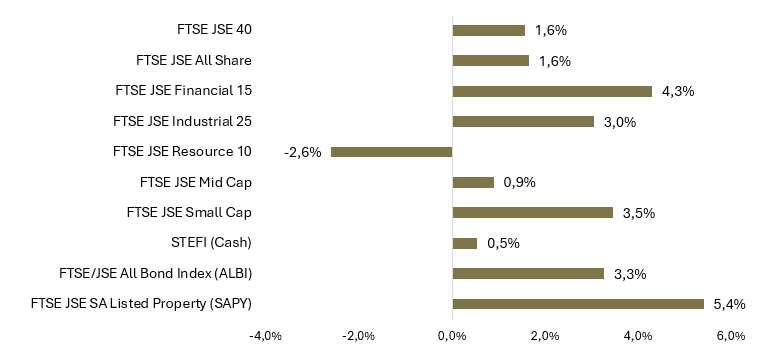

Exhibit 1 | Local Performance (ZAR) for April 2026

Source: Factset. Data as at 30 April 2026. Past performance is not indicative of future performance. For illustrative purposes only and not indicative of any investment.

South Africa

Economy

South Africa’s inflation data remained benign in March, with headline inflation (CPI) printing at 3.1% year‑on‑year, broadly in line with expectations and close to the South African Reserve Bank’s (SARB’s) revised 3% target. However, this data still reflects a period before the full impact of elevated global energy prices filters through to domestic fuel and transport costs.

Against this backdrop, the SARB is expected to remain cautious in coming months. While inflation remains contained for now, persistently higher oil prices pose upside risks that could limit scope for policy easing and potentially revive rate‑hike concerns should second‑round effects emerge.

Equity Markets

South African equities delivered modest gains in April. The FTSE/JSE All Share Index (ALSI) rose 1.6% month‑on‑month, lifting the market back into slightly positive territory for the year (+1.2% year to date). Performance, however, lagged the strong rally seen in global equities.

Sector performance was mixed:

- Banks were among the strongest contributors, rising around 4% on improved global risk sentiment, a firmer rand and easing pressure on local bond yields.

- Listed property also recovered, gaining over 5%, supported by the decline in the SA 10‑year government yield to below 9%.

- Diversified miners delivered solid gains, with counters such as Anglo American and BHP Group benefiting from a rebound in industrial metals, particularly copper.

- In contrast, precious‑metal miners detracted meaningfully from performance as gold and platinum prices declined for a second consecutive month.

Overall, April’s equity performance highlighted the JSE All Share’s structural exposure to commodities and offshore holdings. While global risk appetite improved significantly, local returns remained capped by precious‑metal weakness and the absence of broad‑based domestic growth momentum.

Best performers:

Sasol Ltd 12.6%

MTN Group 8.8%

Investec 8.5%

Anglo American 8.5%

Standard Bank 7.0%

Worst performers:

Goldfields Ltd – 12.6%

Clicks Group – 11.5%

Anglo Gold Ashanti – 10.2%

Northam Platinum – 8.2%

Pan African Resource – 7.1%

Bond Market and Currency

The rand strengthened by approximately 1.6% against the US dollar in April, supported by improved global risk appetite and a softer dollar. Despite the monthly recovery, the currency remains marginally weaker year‑to‑date.

Local bond markets also stabilised. The South African 10‑year government yield declined to around 8.9%, as easing risk aversion and a stronger rand offset concerns around global inflation and higher energy prices. Notably, local bonds outperformed many global peers during the month, despite higher yields offshore.

GLOBAL MARKETS

April marked a decisive shift in market sentiment. Investors looked past ongoing geopolitical uncertainty to focus on improving earnings momentum, stabilising inflation expectations and the prospect of policy rates remaining on hold rather than moving materially higher. The result was one of the strongest monthly rallies in global equities in several years.

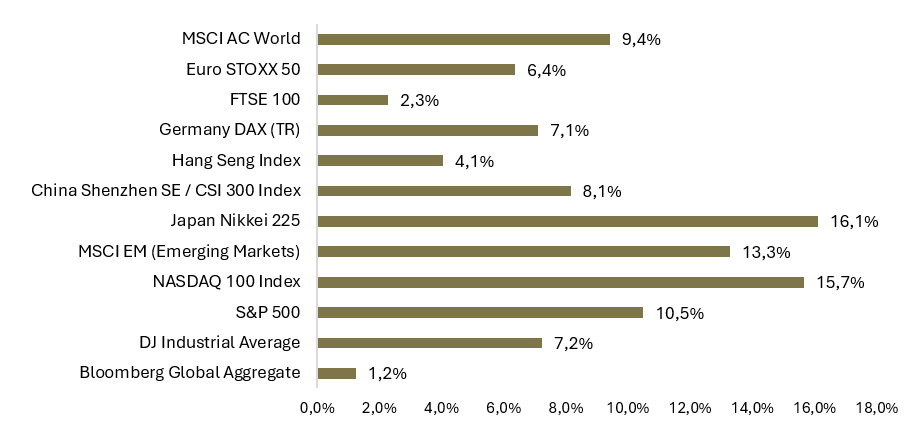

Exhibit 2 | Global Performance (base currency) April 2026

Source: Factset. Data as at 30 April 2026. Past performance is not indicative of future performance. For illustrative purposes only and not indicative of any investment.

United States

US equities led the global rebound. The S&P 500 gained over 10%, while the Nasdaq 100 surged over 15%, driven by strong performance from mega‑cap technology and AI‑linked stocks.

Technology heavyweights delivered particularly strong results, with cloud computing and AI‑related demand continuing to surprise to the upside.

At its April meeting, the US Federal Reserve kept interest rates unchanged. While the accompanying statement carried a slightly hawkish tone, markets interpreted the decision as confirmation that policy would remain restrictive but stable, rather than tightening further in the near term.

Europe

European equity markets participated in the rebound but underperformed the US and Asia. Ongoing energy‑supply disruptions and softer business‑activity data capped gains, particularly in economies most exposed to higher energy costs. Purchasing Managers’ Indices pointed to weakening momentum, suggesting that elevated input costs continue to weigh on activity.

Investor sentiment in the region remained sensitive to developments in energy markets, with the rebound proving more tentative than in regions more directly exposed to global technology and growth themes.

United Kingdom

The UK market lagged global peers in April. The UK equity markets structural tilt toward energy, financials and defensive stocks worked against it in a month dominated by growth and technology leadership. Energy stocks were volatile as oil prices swung sharply during the month, while persistent inflation pressures kept expectations for Bank of England policy relatively tight.

Asia

Asian equity markets were among the strongest performers globally in April and deserve distinct treatment this month. Gains were overwhelmingly concentrated in North Asia, particularly Taiwan and South Korea, where markets surged as investors rotated decisively back into the global AI semiconductor supply chain.

Technology hardware and semiconductor stocks delivered exceptional returns, reflecting renewed confidence in AI‑related capital expenditure and strong demand for data‑centre and chip infrastructure. The rally was broad within these markets, extending beyond a handful of large names and signalling a material shift back toward risk‑on positioning in the region.

Japan also posted positive returns, although gains were more modest. While Japan participated in the global rebound, its more limited direct exposure to the AI theme and continued sensitivity to energy prices constrained relative performance.

Emerging Markets (EM)

Emerging market equities delivered a strong rebound in April, but performance across the asset class was far from uniform. The MSCI Emerging Markets Index rose sharply, largely driven by outsized gains in Asian markets linked to the global technology and semiconductor cycle.

Outside Asia, performance was more mixed. Latin American markets proved relatively resilient, supported by commodity exposure and improved risk appetite, although gains were more measured than in EM Asia. Middle Eastern markets continued to face headwinds from regional geopolitical uncertainty, while parts of EM EMEA lagged as higher energy prices and tighter financial conditions weighed on growth expectations.

Overall, April highlighted the importance of regional and thematic differentiation within emerging markets, with performance heavily skewed toward countries most exposed to global technology and growth trends.

Commodities and Currencies

Commodity markets delivered mixed performance. Energy prices remained volatile, with Brent Crude (oil) experiencing large intra‑month swings before ending April slightly lower monthly. Despite the pullback, oil prices remain elevated, sustaining inflation risks.

Industrial metals strengthened, supported by improved growth expectations and AI‑related infrastructure demand. Gold, however, declined again, as easing risk aversion and firmer real yields reduced demand for traditional safe‑haven assets.

The US dollar weakened against most major currencies, reflecting improved global sentiment and a partial unwind of March’s flight‑to‑safety positioning.

Outlook

April demonstrated how quickly market sentiment can shift. Following the sharp repricing of risk in March, investors responded decisively to signs of de‑escalation, resilient earnings and stable policy settings. While geopolitical risks remain elevated and energy prices continue to pose upside inflation risks, markets have shown a renewed willingness to focus on fundamentals.

For South Africa, the environment remains finely balanced. Global risk appetite and a softer dollar provide support for local assets, but commodity‑price volatility and the lagged impact of higher fuel costs on inflation warrant caution. In this context, maintaining diversification across asset classes and regions remains essential, particularly as markets continue to oscillate between optimism and uncertainty.