Global markets delivered a mixed but resilient performance in February. Equities oscillated between losses and rebounds as investors weighed the scale of artificial intelligence (AI)‑related investment, uncertainty around US trade and tariff policy, and an escalation in Middle East tensions. While technology shares came under pressure and US indices ended the month mostly softer, Europe, Japan and commodity‑linked markets advanced, supported by firmer data and strong resource prices.

Locally, South African assets extended their strong run. The FTSE/JSE All Share Index (ALSI) gained around 7% in February, marking a twelfth consecutive positive month and reflecting renewed strength in resources, solid gains in financials and property, and a firmer rand.

LOCAL MARKETS

Exhibit 1 | Local Performance (ZAR) for February 2026

Source: Factset. Data as at 28 February 2026. Past performance is not indicative of future performance. For illustrative purposes only and not indicative of any investment.

South Africa

Economy

South Africa’s macroeconomic backdrop remained broadly stable in early 2026. Headline consumer inflation for January eased slightly to 3.5% year‑on‑year, from 3.6% in December, primarily on the back of lower fuel costs. Core inflation ticked up to 3.4% from 3.3% but remains close to the lower end of the SARB’s 3 – 6% target band, underscoring a relatively gentle inflation environment.

South Africa’s short‑term economic data was mixed. Retail sales grew 2.6% year‑on‑year in December, slightly slower than November’s revised 3.6%, showing that consumers remain under pressure, but spending has not collapsed. Labour market data was a little more encouraging as the latest Quarterly Labour Force Survey showed the unemployment rate improving to 31.4% in the fourth quarter of 2025, from 31.9% in the previous quarter, as the number of unemployed people declined modestly.

The 2026 National Budget, tabled on 25 February, was broadly well received by markets. Treasury reaffirmed its commitment to fiscal consolidation, projecting that the debt‑to‑GDP ratio will peak this year at 78.9% before gradually declining. Stronger‑than‑expected revenue, helped by elevated gold and platinum prices, allowed government to avoid significant tax hikes, while maintaining a measured, pragmatic stance on expenditure. The combination of commodity‑driven revenue support and improved discipline has strengthened confidence in South Africa’s medium‑term fiscal trajectory.

Equity Markets

South African equities delivered another strong month in February. The FTSE/JSE All Share Index (ALSI) rose approximately 7.0%, extending its winning streak to a twelfth consecutive positive month and again ranking among the stronger emerging market performers.

Sector performance remained highly differentiated:

- Resources advanced around 13.4%, continuing to dominate the market as precious metal and diversified miners benefited from another powerful rally in gold and platinum group metals, as well as firmer energy prices.

- Financials gained roughly 7.4%, supported by solid bank updates, improved risk sentiment toward South Africa and the supportive backdrop of high real yields.

- The SA Listed Property Index (SAPY) rose about 6.3%, as stable long‑bond yields and better perceptions of South Africa’s fiscal trajectory underpinned the asset class.

- Industrials were broadly flat at around ‑0.1%, with weakness in large rand‑hedge and technology‑linked holdings offsetting gains elsewhere in the sector.

Performance at the stock level was again overwhelmingly driven by commodity‑linked counters, particularly gold and energy names. On the downside, February proved challenging for several consumer‑facing retailers and tech/investment holdings that are less tied to commodities and global cyclicals.

Best performers:

AngloGold Ashanti 30.33%

Sasol Ltd 27.16%

Valterra Platinum Ltd 22.66%

Nedbank Group Ltd 18.72%

BHP Group Limited 16.27%

Worst performers:

Prosus NV – 11.63%

Naspers – 10.71%

Sibanye Stillwater Ltd – 5.12%

Clicks Group – 2.23%

Harmony Gold Mining – 1.34%

Bond Market:

Local fixed income delivered positive returns across both nominal and inflation‑linked bonds in February. The FTSE/JSE All Bond Index (ALBI) returned 1.74% for the month, while the composite inflation‑linked bond index (CILI) gained 3.51%. Longer‑dated nominal yields moved lower, with the curve flattening as the R2048 yield fell more sharply than the R2030.

The rand extended its appreciation trend, supported by strong resource prices, ongoing foreign interest in local assets and a broadly constructive emerging‑market backdrop. The USD/ZAR strengthened by about 1.3% over the month to close near R15.92/US$, while the euro and pound also eased modestly against the rand. Despite intermittent volatility linked to global risk events, South African bonds and the currency continue to benefit from high real yields, improving fiscal metrics and comparatively attractive valuations versus many peers.

GLOBAL MARKETS

Global markets delivered a mixed but resilient performance in February. Equity indices swung between gains and pullbacks as investors balanced large AI‑related capital expenditure announcements, shifting US tariff policy, and rising geopolitical tensions in the Middle East. Despite pressures on global technology shares, strength in resources, energy, and selected cyclical sectors helped support overall market performance, while Europe and Japan posted notable gains against a backdrop of moderating inflation and improving economic indicators. Emerging markets, including South Africa, remained firm beneficiaries of rising commodity prices and stable risk appetite.

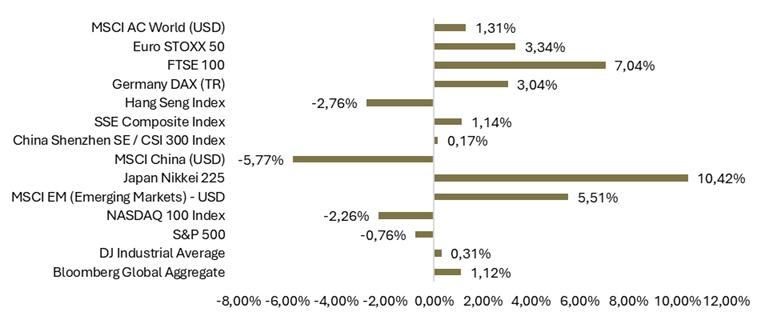

Exhibit 2 | Global Performance (base currency) February 2026

Source: Factset. Data as at 28 February 2026. Past performance is not indicative of future performance. For illustrative purposes only and not indicative of any investment.

United States

Global markets spent much of February grappling with the scale and sustainability of AI‑related investment. Major US technology companies unveiled 2026 capex plans implying AI‑linked investment of around US$650bn, up from an estimated US$450bn in 2025. While AI demand continues to surprise to the upside, supporting cloud platforms and semiconductor manufacturers, investor focus has shifted toward return discipline, differentiating between companies translating capex into durable earnings growth and those primarily expanding spending.

US equity performance reflected this reassessment. The S&P 500 fell roughly 0.8% month-on-month, the Nasdaq declined about 2.26% month-on-month, and the Dow Jones Industrial Average had a 0.3% month-on-month gain, marking its tenth consecutive positive month.

Within the market, mega‑cap technology and growth names generally underperformed, while more cyclically oriented segments – including industrials, financials and defence – showed greater resilience, especially toward month‑end as geopolitical risks intensified.

The Federal Reserve’s January meeting minutes revealed a committee still more concerned about inflation risks staying above target than about labour market softness. There was no clear consensus on the timing of rate cuts, reinforcing the message that policy will remain data‑dependent. Meanwhile, the US Supreme Court struck down key elements of President Trump’s earlier “Liberation Day” tariffs, prompting the administration to pivot to a simpler 10% blanket tariff on all imports – a shift that maintains trade‑related uncertainty even as some legal risks recede.

Europe

European equities extended their year‑to‑date gains in February, benefiting from improving macro data and capital flows seeking diversification away from US tech concentration. The Euro Stoxx 50 rose around 3.3% MoM, while France’s CAC 40 and Germany’s DAX gained approximately 5.6% and 3.0%, respectively.

Eurozone inflation continued to trend lower, with annual CPI at 1.7% in January, down from 1.9% in December, while leading indicators such as manufacturing PMIs improved across several core economies. This combination of moderating inflation and stable growth has allowed the European Central Bank to keep policy rates unchanged, emphasising a resilient economy and inflation gradually converging toward its 2% target.

At the country level, French and Italian manufacturing PMIs moved further into expansion territory, while Germany’s PMI and labour market data surprised to the upside despite softer retail sales. Overall, the region’s outlook remains cautious but improving, with fiscal support and recovering industrial activity underpinning equity performance.

United Kingdom

The UK was one of the stronger developed markets in February. The FTSE 100 climbed around 7.0% month-on-month (+10.2% year-to-date), reaching fresh record highs as energy, financial and select consumer names rallied.

Inflation moderated further. January CPI slowed to roughly 3.0% year-on-year from 3.4% in December – the lowest rate since early 2025 – while core inflation eased to 3.1% from 3.2%. GDP growth remained modest, with 4Q25 output expanding by about 0.1%, in line with the previous quarter and translating into full‑year growth of roughly 1.3%. Against this backdrop, the Bank of England voted narrowly to keep rates on hold at 3.75%, balancing persistent inflation pressures against signs of slower underlying activity.

Asia

Performance across Asia diverged in February. In China, equity markets were relatively subdued. The Shanghai Composite gained around 1.1% month-on-month (+5.0% year-to-date), while Hong Kong’s Hang Seng fell about 2.8% month-on-month. Investors remained cautious ahead of key policy events, including the National People’s Congress (NPC), where expectations centre on further fiscal stimulus and targeted support for consumption and strategic sectors. While economic data show pockets of resilience, concerns linger around the property sector, domestic demand and regulatory uncertainty in parts of the technology complex.

Japan again stood out as a top performer. The Nikkei 225 surged roughly 10.4% month-on-month, reaching new all‑time highs as investors rotated into domestic cyclicals, financials and companies leveraged to AI‑related supply chains. A sharp deceleration in inflation – with headline CPI falling to 1.5% in January from 2.1% – has reinforced expectations that Bank of Japan policy normalisation will remain very gradual, supporting risk appetite.

Emerging Markets (EM)

Emerging market equities outperformed developed peers for a second consecutive month, supported by:

- Strong gains in commodity exporters such as South Africa and Brazil;

- Ongoing strength in semiconductor and AI‑linked manufacturers;

- A constructive backdrop for EM currencies amid modest US dollar weakness earlier in the year.

In ZAR terms, EM equities gained around 4.7% in February, considerably ahead of developed market peers, while S.A. equities delivered one of the best performances within the EM universe.

Commodities and Currencies

Commodities strengthened as geopolitical risks escalated. Brent crude rose roughly 2.5% month-on-month and more than 19% year‑to‑date, briefly trading above US$70–80/bbl as tensions between the US and Iran raised the risk of disruptions through the Strait of Hormuz.

Gold rallied about 7.9% month-on-month (+22.2% year-to-date), reaching new record highs above US$5,000/oz as investors sought safe‑haven assets against a backdrop of geopolitical uncertainty, questions around policy direction and ongoing concerns about central bank independence.

Platinum group metals (PGMs) posted solid gains: platinum and rhodium both advanced high‑single‑digits, while palladium delivered mid‑single‑digit gains, reinforcing the positive sentiment toward resource‑heavy markets and providing a powerful tailwind for South African PGM producers.

Base metals were more mixed: copper and aluminium saw periods of strength on AI‑linked demand and supply constraints, but also experienced bouts of profit‑taking as global growth expectations were recalibrated.

In currencies, the US dollar was somewhat firmer on the month but remains weaker year‑to‑date. The rand nevertheless appreciated against the dollar in February, supported by strong commodity prices, improved domestic fundamentals and ongoing interest in high‑yielding EM assets.

Outlook

February highlighted how sensitive markets remain to AI narratives, policy signals and geopolitics. Questions around the scale and payoff of AI‑related capex, renewed trade and tariff uncertainty, and the escalation of tensions in the Middle East drove short‑term volatility across asset classes. Nevertheless, the underlying macro picture remains broadly constructive.

Inflation continues to moderate in many major economies, even if core measures remain above target. Policy rates appear to be at, or near, cyclical peaks in most regions, with markets anticipating a gradual easing once central banks are confident inflation is on a sustainable path toward the target.

For South Africa, the combination of a credible fiscal consolidation path, with debt projected to peak and then decline, a more favourable inflation outlook – with headline CPI expected to average close to the 3 – 3.5% range over the medium term – high real yields in local bonds, and a powerful commodity tailwind provides a supportive backdrop for local assets. This is the case even as meaningful structural challenges around growth, infrastructure and employment remain firmly in place.

In this environment, we continue to see value in disciplined diversification and balanced portfolio construction. Within equities, a combination of structural growth themes (such as AI and digitalisation) alongside cyclical and value‑oriented sectors (including financials, energy and selected commodities) remains appropriate. In fixed income, South African and broader emerging‑market bonds still offer attractive long‑term opportunities, particularly as inflation expectations become better anchored and fiscal trajectories stabilise.

Short‑term market moves are likely to remain sensitive to news‑flow and policy developments. However, the combination of improving global growth prospects, still‑supportive financial conditions, and ongoing reform and fiscal progress in South Africa provides a constructive foundation for long‑term investors. Maintaining a well‑diversified, quality‑focused approach remains the most effective way to navigate what is likely to be another eventful year for markets.