Global markets in June were defined by de-escalation and rotation. A ceasefire framework between the US and Iran, including the reopening of the Strait of Hormuz to commercial shipping, drove a sharp retreat in oil and precious metal prices. This also eased energy-driven inflation fears that had dominated the first half of the year. Beneath the calmer surface, equity market drivers rotated decisively out of technology and AI-linked names into value and cyclical sectors, with the Dow Jones setting record highs even as the Nasdaq declined. Emerging markets gave back modest ground as Chinese and Hong Kong equities sold off, with commodity-heavy markets such as South Africa among the laggards.

South African assets had a difficult June. The JSE All Share Index closed the month lower once again, dragged down by precious metal miners as gold and platinum prices slumped, capping the market’s weakest quarter in more than two years. In contrast, the rand firmed against the US dollar and local bond yields moved lower, supported by the pullback in oil prices and improving inflation sentiment. The South African Reserve Bank (SARB) did not meet in June, leaving the repo rate at 7.0% following May’s hike, with the next decision scheduled for 23 July. May CPI, released mid-month, accelerated to 4.5%.

LOCAL MARKETS

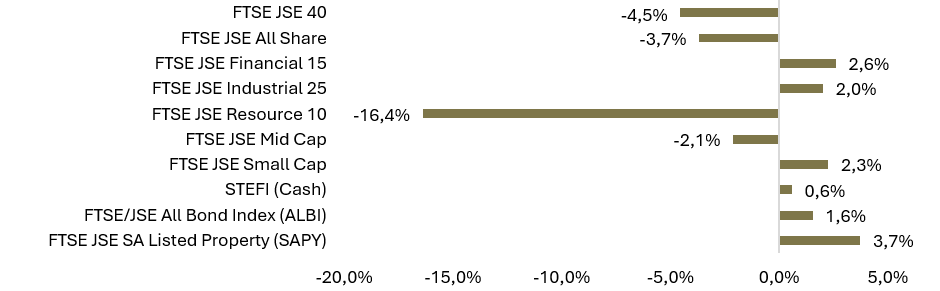

Exhibit 1 | Local Performance (ZAR) for June 2026

South Africa

Economy

South Africa’s inflation continued to climb. Annual consumer inflation rose to 4.5% in May (from 4.0% in April) and reached the highest print since July 2024, while also moving further from the SARB’s 3.0% target. The increase was driven primarily by transport costs, which rose 9.4% year-on-year as higher fuel prices filtered through to consumers. Housing and utilities also contributed following Eskom’s electricity tariff increase. Meanwhile, core inflation edged up to 3.8%. On the growth front, first-quarter GDP expanded by 0.5% (quarter-on-quarter), exceeding the expected 0.3% and introducing the sixth consecutive quarter of expansion.

With no Monetary Policy Committee (MPC) meeting scheduled in June, the repo rate remained unchanged at 7.0%, leaving the prime lending rate at 10.5%. Nonetheless, the SARB’s second-quarter survey showed average 2026 inflation expectations rising sharply from 3.6% to 4.4%. Combined with administered utility tariff increases taking effect from 1 July, the focus remains firmly on the 23 July rate decision, even as falling oil prices point to some relief in fuel prices in the months ahead.

South African equities ended June lower. The FTSE/JSE All Share Index (ALSI) declined by -3.7%, capping its worst quarter in more than two years as precious metal miners slumped alongside sharply lower gold and platinum prices. The Resource 10 index plunged -16.4% in the month, while financials (+2.6%), industrials (+2.0%), small caps (+2.3%) and listed property (+3.7%) all delivered positive returns. This is also a stark example of the divergence between the resource sector and the domestically focused market.

Sector performance was mixed:

- Precious metal miners were the main drag. Several gold and platinum-group miners fell more than 25% as gold recorded its sharpest quarterly drop in 13 years.

- Domestically focused sectors proved resilient, with the Financial 15 (+2.6%), Industrial 25 (+2.0%) and small caps (+2.3%) all posting gains, supported by a firmer rand, lower bond yields and better-than-expected first-quarter GDP data. Retail and financials led the gains, along with listed property (SAPY), which was a standout, returning +3.7%.

- South Africa underperformed within emerging markets once again, with the ALSI’s -3.7% decline well behind the MSCI EM Index’s more modest -1.4% pullback.

Overall, June’s equity performance again underlined the JSE’s structural sensitivity to precious metal prices. Notably, the sell-off has left South African equities trading at a discount of close to 19% to its emerging market peers on forward earnings. A Bank of America survey, conducted during the month, showed the highest share of local fund managers seeing more buying than selling opportunities since 2009 – suggesting that longer-term value may be emerging from the current weakness.

Best performers:

Mr Price Group: 15.0%

Bid Corp: 9.8%

Richemont: 8.1%

Capitec: 6.5%

FirstRand: 5.3%

Worst performers:

Pan African Resources: – 29.1%

Sibanye-Stillwater: – 28.7%

Impala Platinum: – 25.8%

Northam Platinum Holdings: – 25.3%

Sasol: – 19.7%

Bond market and currency

The rand firmed in June, supported by a pullback in oil prices, better-than-expected domestic growth data, and improved emerging-market sentiment as the US-Iran ceasefire took hold. At the end of the month, the USD/ZAR rate was trading around R16.3, with the euro at R18.7 and the British pound at R21.8. The rand tugged between the R16.2-R16.7 range during the month and strengthened further into early July (even in the face of a firmer US dollar globally).

Local bond markets delivered positive returns in June. The SA 10-year bond yield declined to around 8.4% (from 8.6% at the end of May), and the 20-year yield eased (from 9.1%) to around 8.9%, as the reopening of the Strait of Hormuz and falling oil prices improved the domestic inflation outlook and led to investors scaling back tightening bets.

The ALBI returned +1.6% for the month, with real yields remaining attractive relative to global peers. That said, the sharp rise in surveyed inflation expectations and the utility tariff increases means the risk of further SARB action remains a possibility ahead of the 23 July MPC meeting.

GLOBAL MARKETS

Global markets delivered mixed but generally resilient returns in June as easing geopolitical tensions shifted investors’ focus back to inflation, interest rates and corporate fundamentals. The sharp fall in oil prices following the Middle East ceasefire helped alleviate energy-related inflation concerns, but expectations of higher-for-longer US interest rates and widespread profit-taking in technology and AI-related shares prompted a significant rotation in market leadership. Value-oriented sectors such as financials, industrials, utilities and healthcare outperformed, lifting the Dow Jones to record highs, while technology-heavy markets lagged. Europe benefited from easing energy costs and softer inflation, Japan continued its strong run despite late-month volatility, and emerging markets delivered mixed returns as weakness in Chinese technology shares offset resilience elsewhere.

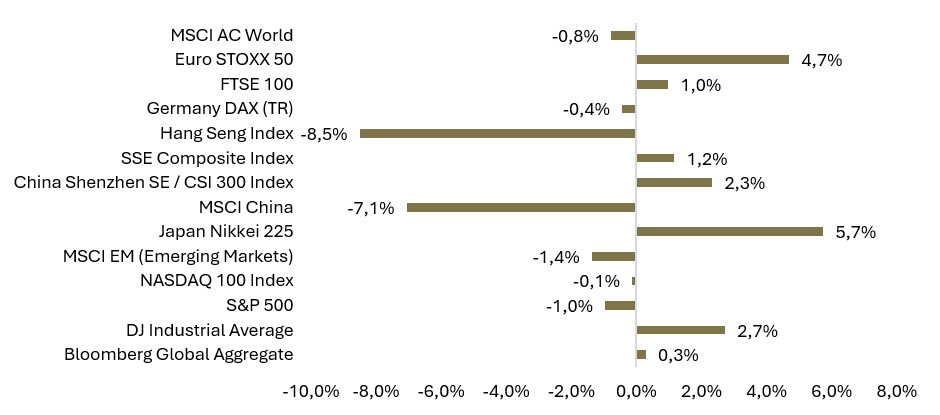

Exhibit 2 | Global Performance (base currency) June 2026

Source: Factset. Data as at 30 June 2026. Past performance is not indicative of future performance. For illustrative purposes only and not indicative of any investment.

United States

US equity markets ended June mixed as a pronounced sector rotation took hold. The S&P 500 declined -1.0%, and the NASDAQ 100 slipped -0.1% as investors took profits in semiconductors and AI-linked names. The Dow Jones Industrial Average gained 2.7%, ending the month at a record close of 52,319.2 – its best first half since 2021.

Rotation into financials, industrials, utilities and healthcare drove the divergence, and the Russell 2000 also reached new highs, capping its strongest first half since 1991. Despite June’s late-month tech weakness, the second quarter (as a whole) was the strongest for US equities since 2020.

Sentiment was supported by the sharp decline in oil prices as the ceasefire took hold, although the inflation picture remained uncomfortable. May CPI, released mid-month, came in at 4.2% year-on-year, which is the fastest annual pace since April 2023. The incline was driven by the surge in energy costs over the past twelve months. Consumer confidence edged higher in June as falling petrol prices lifted spirits, even as labour market concerns intensified.

The US Federal Reserve held rates steady at 3.5%-3.8% at the June Federal Open Market Committee (FOMC) meeting – the first under newly confirmed Chair Kevin Warsh – in a decision widely read as a renewed commitment to containing inflation.

Expectations of near-term rate cuts remained firmly off the table, with markets instead pricing a meaningful possibility of a hike later in 2026. The hawkish repricing lifted the US dollar index by around 2.4% to a one-year high, weighing heavily on gold and other non-yielding assets.

Europe

European equity markets posted solid gains in June. The Euro STOXX 50 rallied 4.7%, while Germany’s DAX (TR) edged -0.4% lower after a strong run in prior months. The region’s heavy energy import dependence (a clear vulnerability highlighted during recent conflict) became a source of relief as oil prices retreated towards pre-conflict levels, easing pressure on industry and household sentiment.

Encouragingly, eurozone inflation eased to 2.8% in June (from 3.2% in May), coming in below the 3.0% expected, as energy price pressures faded and inflation slowed across Germany, France and Italy. Although the headline rate remains above the European Central Bank’s (ECB) 2.0% target, the improving trend reduces the urgency for further policy action, and the ECB maintained its cautious, data-dependent stance through the month.

United Kingdom

The UK market ended June modestly higher, with the FTSE 100 gaining 1.0% as investors rotated away from technology towards value-oriented sectors. The Bank of England (BoE) voted 7-2 to keep interest rates unchanged at 3.8%, with annual inflation steady at 2.8% in May. Governor Andrew Bailey cautioned that inflation could rise towards 3.2% before heading lower. This is, in part, because the household energy price cap reset from July will pass earlier oil price increases through to consumers – leaving the Bank balancing sticky inflation against sluggish growth.

Asia

Asian markets were volatile in June. In Japan, the Nikkei 225 gained 5.7%, climbing to fresh record highs around the 70,000 level mid-month before a sharp, technology-led sell-off in the final week. The move was triggered by profit-taking in AI and semiconductor names and reports of a possible OpenAI IPO delay. Domestically, the Bank of Japan’s (BoJ) Tankan survey showed large-manufacturer sentiment improving for a fifth consecutive quarter, and rising bond yields supporting financials and other cyclical sectors.

Hong Kong was the weakest major market, with the Hang Seng Index falling -8.5% and MSCI China down -7.1%, as the technology sell-off hit the region’s heavyweight internet and AI-linked names hardest. Mainland onshore markets held up far better – the SSE Composite gained 1.2%, and the CSI 300 rose 2.3% – helped by an improvement in China’s official measure of factory activity, which pointed to continued resilience in parts of the Chinese economy.

Emerging Markets (EM)

Emerging market equities paused in June, with the MSCI Emerging Markets Index slipping -1.4% as the sell-off in Chinese and Hong Kong technology names weighed on the asset class’s largest constituents. The modest monthly decline follows an exceptionally strong run, however – the index remains up 44.2% over the past twelve months, comfortably ahead of developed market peers.

Returns across the region were uneven. South Korea saw sharp swings late in the month as the global sell-off in AI and chip stocks spilt over, though the market remained well up for the year. South Africa lagged the broader index, with the slump in precious metals dragging the JSE to a -3.7% decline against the EM benchmark’s -1.4%.

Overall, June again reinforced the importance of regional differentiation within emerging markets. Energy importers benefited directly from falling oil prices. Technology-heavy markets such as Hong Kong bore the brunt of the AI profit-taking. Precious-metal exporters, such as South Africa, lagged as precious metals sectors corrected.

Commodities and currencies

Commodity markets were dominated by the unwinding of the energy shock in June. Brent crude fell steeply with a decline of roughly -20.0% to end the month at around $72/bbl (back to near pre-conflict levels). The 60-day ceasefire, the reopening of the Strait of Hormuz, the UAE’s departure from OPEC, and strategic petroleum reserve releases all contributed to the downward pressure. The retreat in oil materially eases inflation pressure globally and locally, although the durability of the ceasefire remains the key risk to this improved picture.

Precious metals sold off sharply in June. Gold fell by around -12% to end the month at approximately $4,018/oz, extending its decline into a fourth consecutive week and recording its steepest quarterly fall in 13 years. The sell-off was driven by hawkish repricing of US Federal Reserve interest rate expectations and a stronger US dollar, which reduced the appeal of non-yielding safe-haven assets.

Platinum fell close to -20% (to around $1,560/oz), and silver dropped more than -21%. Copper proved far more resilient, easing only around -3.0% from May’s record highs, as tight concentrate supply and structural demand continued to underpin the market.

Currency markets reflected the hawkish shift in US rate expectations, with the US dollar index rising by around 2.4% in June to a one-year high. Emerging market currencies held up well, and the rand was a relative outperformer. The USD/ZAR rate ended the month at around R16.3, with the euro at R18.7 and the British pound at R21.8. The euro traded at around $1.1 against the dollar at month-end.

Outlook

The macro narrative shifted meaningfully in June from energy shock to tentative de-escalation. With Brent crude back near pre-conflict levels and the Strait of Hormuz reopened under the ceasefire framework, the inflation outlook has improved, and lower fuel prices should begin to pass through to headline inflation prints in the months ahead.

Central banks remain firmly cautious: the damage from the energy shock is still working through the system, inflation remains above target across most major economies, and markets are now pricing the possibility of a US rate hike rather than cuts in 2026. The durability of the ceasefire – and continued free passage through the Strait of Hormuz – is the single most important variable for markets heading into the second half of the year.

For South Africa, July brings the SARB’s 23 July MPC meeting into sharp focus. The committee faces a two-sided picture. Falling oil prices point to fuel price relief and an improving inflation trajectory. However, surveyed inflation expectations have risen well above target, administered utility tariffs increased from 1 July, and food price risks (from higher fertiliser costs and potential El Niño-related drought conditions) loom in the second half of the year.

The JSE’s structural exposure to precious metals remains the swing factor for equity returns, and further weakness in gold and platinum prices would continue to weigh on the resource-heavy index. Local valuations now sit at a substantial discount to emerging market peers, and domestic fund manager sentiment is at its most constructive in over a decade – a reminder that weakness can create opportunity.

In this environment, maintaining broad diversification across asset classes and regions remains essential. Quality, resilience and disciplined portfolio construction continue to be the most effective tools for navigating what remains an uncertain and event-driven market backdrop.