Global markets navigated a complex and cautious May, as investor sentiment revolved around the prospect of US-Iran peace talks and their potential implications for energy prices and inflation. While hopes for a diplomatic resolution lent some support to risk assets – particularly in consumer, retail and leisure sectors – underlying uncertainty remained elevated. Oil prices stayed volatile, and markets remained sensitive to any shift in geopolitical developments. Equity performance was mixed across regions, with the US and UK ending marginally higher while parts of Asia traded under pressure.

South African assets delivered a mixed performance in May. The JSE All Share Index closed the month modestly lower, weighed down by losses in investment holding companies and property stocks. Gold and platinum miners also came under pressure. The rand showed some resilience against a backdrop of dollar volatility, and local bond yields moved lower, providing a degree of support to fixed-income investors. At the end of the month (28 May), the South African Reserve Bank (SARB) announced a 25bps rate hike.

LOCAL MARKETS

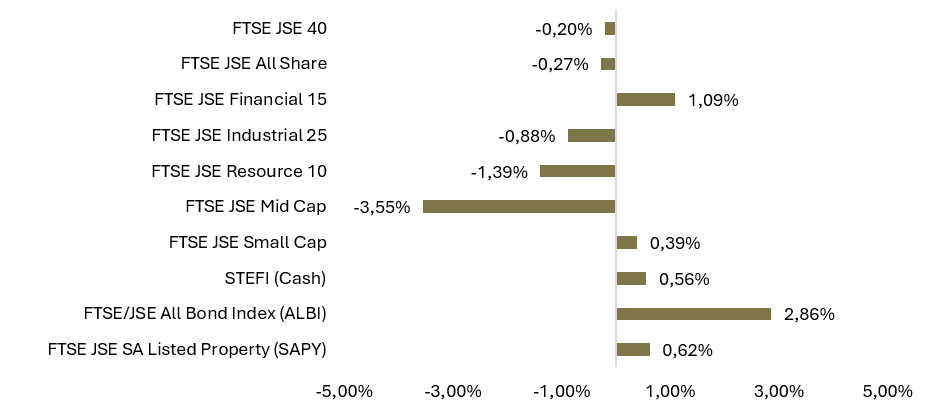

Exhibit 1 | Local Performance (ZAR) for May 2026

Source: Factset. Data as at 02 June 2026. Past performance is not indicative of future performance. For illustrative purposes only and not indicative of any investment.

South Africa

Economy

South Africa’s inflation picture remained broadly contained entering May, with April CPI data coming out at 4.00%. Despite the increase, it was still close to the South African Reserve Bank’s (SARB’s) 3.00% target. However, the ongoing volatility in global oil prices – driven by the conflict between the US-Israel coalition and Iran, and associated risks to Strait of Hormuz supply routes – continued to pose upside risks to domestic fuel and transport costs in the months ahead. Against this backdrop, the SARB hiked rates by 25bps, pushing the repo rate to 7.00% and the prime lending rate to 10.50%.

Equity Markets

South African equities printed a flat performance. The FTSE/JSE All Share Index (ALSI) closed the month slightly lower, weighed down by losses across investment holding companies, property stocks, and precious metal miners. Telecommunications names provided some offset, with Telkom and Vodacom among the brighter spots.

Sector performance was mixed:

- Investment holding companies were among the weakest performers, with Reinet Investments and Hosken Consolidated Investments declining sharply in the month.

- Listed property came under renewed pressure, with real estate investment trusts ending the month lower.

- Telecommunications names provided a bright spot, with Telkom SA SOC surging strongly and Vodacom Group also advancing, supported by improved domestic sentiment.

- Precious metal miners detracted from performance once again, as gold and platinum prices remained under pressure.

Overall, May’s equity performance reflected the JSE All Share’s continued sensitivity to geopolitical developments and commodity price movements. Ongoing uncertainty surrounding the geopolitical conflict and its implications for oil and precious metal prices weighed on the resource-heavy index, while the absence of a broad domestic growth catalyst left the market vulnerable to external headwinds.

Best performers:

Harmony Gold Mining: 12.41%

Richemont: 10.78%

BHP Group Limited: 9.48%

Anglo American: 7.78%

Vodacom Group Ltd: 7.73%

Worst performers:

Reinet Investments SCA: – 14.76%

Sasol: – 12.46%

Clicks Group: – 10.75%

Goldfields Ltd: – 9.91%

Prosus NV: – 8.25%

Bond Market and Currency

The rand showed resilience in May, broadly holding its ground against the US dollar against a backdrop of geopolitical uncertainty. At the end of the month, the USD/ZAR rate was trading around R16.47, with the euro at R19.11 and the British pound at R22.05. While intermittent dollar strength posed headwinds, improved sentiment around US-Iran peace talks provided periodic support for emerging market currencies, including the rand.

Local bond markets delivered positive returns in May. The SA 10-year bond yield declined to 8.64%, while the 20-year yield eased to 9.11%, reflecting improved sentiment and some easing of global risk aversion as oil prices retreated from their earlier highs. The ALBI was positive for the month, with real yields remaining attractive relative to global peers. The coming months could see a cooling off or even a reversal of these bond performance metrics due to the May rate hike.

GLOBAL MARKETS

May was a month defined by geopolitical tension and cautious optimism. The ongoing conflict and associated risks around oil supply remained the dominant macro theme, keeping energy prices elevated and inflation expectations unsettled. However, emerging signals of progress in peace talks provided intermittent relief, lifting risk appetite in consumer and leisure sectors. Global equity markets ended the month with a mixed picture – the US and UK edged modestly higher, while parts of Asia traded under pressure.

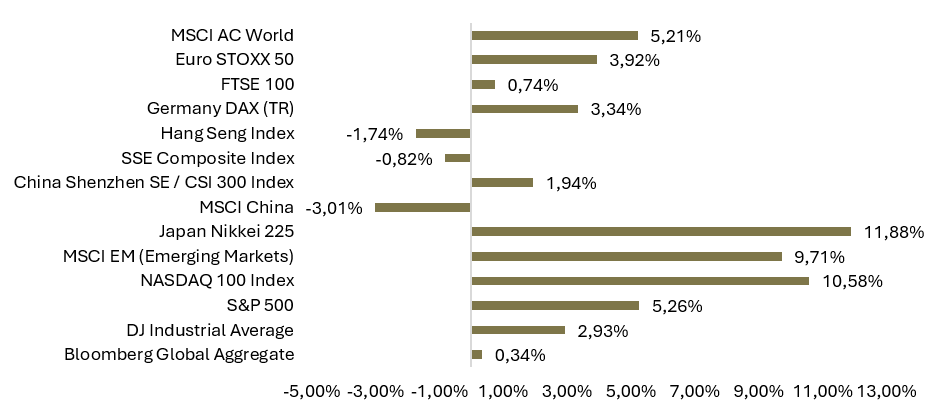

Exhibit 2 | Global Performance (base currency) May 2026

Source: Factset. Data as at 02 June 2026. Past performance is not indicative of future performance. For illustrative purposes only and not indicative of any investment.

United States

US equity markets ended May marginally higher, buoyed by optimism around peace negotiations and resilient consumer spending. The S&P 500 ended higher at 5.26%, while the Dow Jones Industrial Average closed at 2.93% and the Nasdaq at 10.58%. Gains were concentrated in consumer-facing and leisure names, with cruise ship operators, casino companies and beverage groups among the notable outperformers.

The broader market sentiment was supported by easing oil prices late in the month, which fell as investors awaited progress in the US–Iran talks, taking some pressure off inflation expectations. The American Petroleum Institute (API) also reported a decline in crude oil inventories, providing further support for energy markets.

The US Federal Reserve held rates steady, maintaining its data-dependent stance as it monitored the inflationary implications of elevated energy prices and the evolving geopolitical backdrop. Rising inflation concerns stemming from the Iran conflict kept expectations of near-term rate cuts firmly off the table, with gold declining as expectations of further US interest rate hikes firmed.

Europe

European equity markets faced a decent month while persistent energy price pressures and geopolitical uncertainty weighed on sentiment. The Euro STOXX 50 and Germany’s DAX printed moderate gains, as the region’s significant energy import dependence left it particularly exposed to the volatility in oil prices stemming from Middle East tensions. Consumer confidence in France deteriorated in May, declining to 82.00 from 84.00 in the prior month, underscoring the ongoing pressure on household sentiment from elevated costs.

Italy’s industrial sales data offered a mild positive surprise, rising 2.00% month-on-month in March. Switzerland’s ZEW expectations index also improved markedly in May, climbing from -30.30 to -11.10, suggesting that business confidence in the region may be beginning to stabilise. The European Central Bank maintained its cautious stance as it continued to assess the inflationary impact of energy price developments.

United Kingdom

The UK market ended May modestly higher, with the FTSE 100 increasing by 0.74%. The market was supported by improved sentiment around geopolitical conflicts. This supported gains across the retail and consumer sectors, with JD Sports Fashion, Marks & Spencer, Burberry and Next all delivering positive returns during the month. Energy utilities, however, faced headwinds as easing oil prices weighed on the sector. The Bank of England maintained its cautious stance, as persistent inflation pressures limited room for policy easing despite signs of moderating underlying activity.

Asia

Asian markets traded mostly lower in May, amid uncertainty over broader Middle East tensions. In Japan, the Nikkei 225 was up by 11.88% in the last month, with performance mixed across sectors. Electronics components manufacturer TDK Corporation advanced strongly, while mining company Sumitomo Metal Mining declined on softer commodity sentiment.

In Hong Kong, the Hang Seng Index declined -1.74%, reflecting cautious sentiment and concerns around the impact of sustained energy price volatility on regional growth. Performance across the region underscored the sensitivity of Asian markets to geopolitical developments and their implications for energy costs and global trade flows.

Emerging Markets (EM)

Emerging market equities faced a mixed month in May, with performance diverging significantly across regions. The MSCI Emerging Markets Index was under pressure as the combination of higher energy prices, a firmer US dollar in risk-off periods, and geopolitical uncertainty weighed on the asset class more broadly.

Asian emerging markets were softer, with Hong Kong and South Korea both declining as noted above. Middle Eastern markets remained under pressure amid the ongoing regional conflict, while commodity-linked economies in Africa and Latin America faced headwinds from lower precious metal prices and energy-price volatility. South Africa underperformed within the EM universe, with weakness in mining and property sectors dragging on overall returns.

Overall, May reinforced the importance of regional differentiation within emerging markets. Geopolitical positioning, energy import exposure, and commodity linkage were the key determinants of relative performance, with markets most sensitive to Middle East developments lagging their peers.

Commodities and Currencies

Commodity markets were dominated by energy price volatility in May. Brent crude oil experienced significant intra-month fluctuations, briefly rallying before reversing sharply to end the month down -15.12%, as investors weighed developments and uncertainty surrounding ongoing peace negotiations. Despite the pullback from the peak, Brent crude remained at elevated levels, sustaining upside risks to inflation globally and locally.

Gold came under pressure in May, declining as rising inflation concerns from the Iran conflict strengthened expectations of further US interest rate hikes, reducing the appeal of non-yielding safe-haven assets. Gold ended the month trading at around $4,495/oz, roughly a -2.65% decline. Base metals were also softer, while copper improved by 5.77%, Platinum fell -3.25%, reflecting concerns around the global growth outlook and the impact of sustained energy price pressures on industrial activity.

Currency markets reflected the push-and-pull of geopolitical risk and peace-talk optimism. The US dollar traded with intermittent strength against emerging market currencies, with the USD/ZAR rate at around R16.28 at the end of the month. The euro slipped against the dollar to trade at $1.1596. The British pound held firmer against the rand at R21.82. Overall, the dollar remained sensitive to developments in the negotiations, with any signs of progress tending to ease safe-haven demand and support risk currencies.

Outlook

The ongoing geopolitical conflicts and associated energy shock continued to dominate the macro narrative, keeping inflation expectations elevated and limiting the scope for central bank easing across most major economies. While tentative signals of diplomatic progress provided intermittent relief and supported risk assets in pockets – particularly in consumer and leisure sectors – the underlying environment remained uncertain. With oil prices still elevated and their full pass-through to domestic inflation yet to materialise, central banks are likely to remain on hold as they assess the evolving situation.

For South Africa, the outlook heading into June remains cautiously restricted. Higher expected local bond yields (following the recent rate hike) and a relatively resilient rand provide some support for domestic assets, while the SARB’s data-dependent stance offers a degree of policy flexibility should global conditions stabilise. However, the JSE’s structural exposure to precious metals and commodity prices means that any further deterioration in geopolitical conditions or sustained weakness in gold and platinum prices could weigh on equity returns. In this environment, maintaining broad diversification across asset classes and regions remains essential. Quality, resilience and disciplined portfolio construction continue to be the most effective tools for navigating what remains an uncertain and event-driven market backdrop.